Constellation Software 2026 AGM Update

On AI, PEMS, Organic Growth, the Law of Large Numbers and Five Lessons from Mark Miller's First AGM as President

In our March update on Constellation Software Inc (TSX: CSU) fiscal 2025 results, we landed on the verdict that the biggest threat to CSI isn’t AI eroding the VMS moat - it’s the gravitational pull of the company’s own success.

To maintain historical growth rates, the company now needs to deploy $1.5–$1.8 billion in capital annually - and that number is only going to go up with time. Buying 200 small companies a year stops moving the needle.

So what comes next for the VMS behemoth?

The 2026 CSI Annual General Meeting, held on May 15, 2026 was the first sustained opportunity for management to walk through that answer in detail. With an estimated $20 billion of free cash flow to redeploy over the next five years, CSI needed to outline its playbook for the coming years.

President Mark Miller’s address - plus the panels that followed - went a long way towards articulating that plan.

Here are the five takeaways that matter most for any long-term CSI holder.

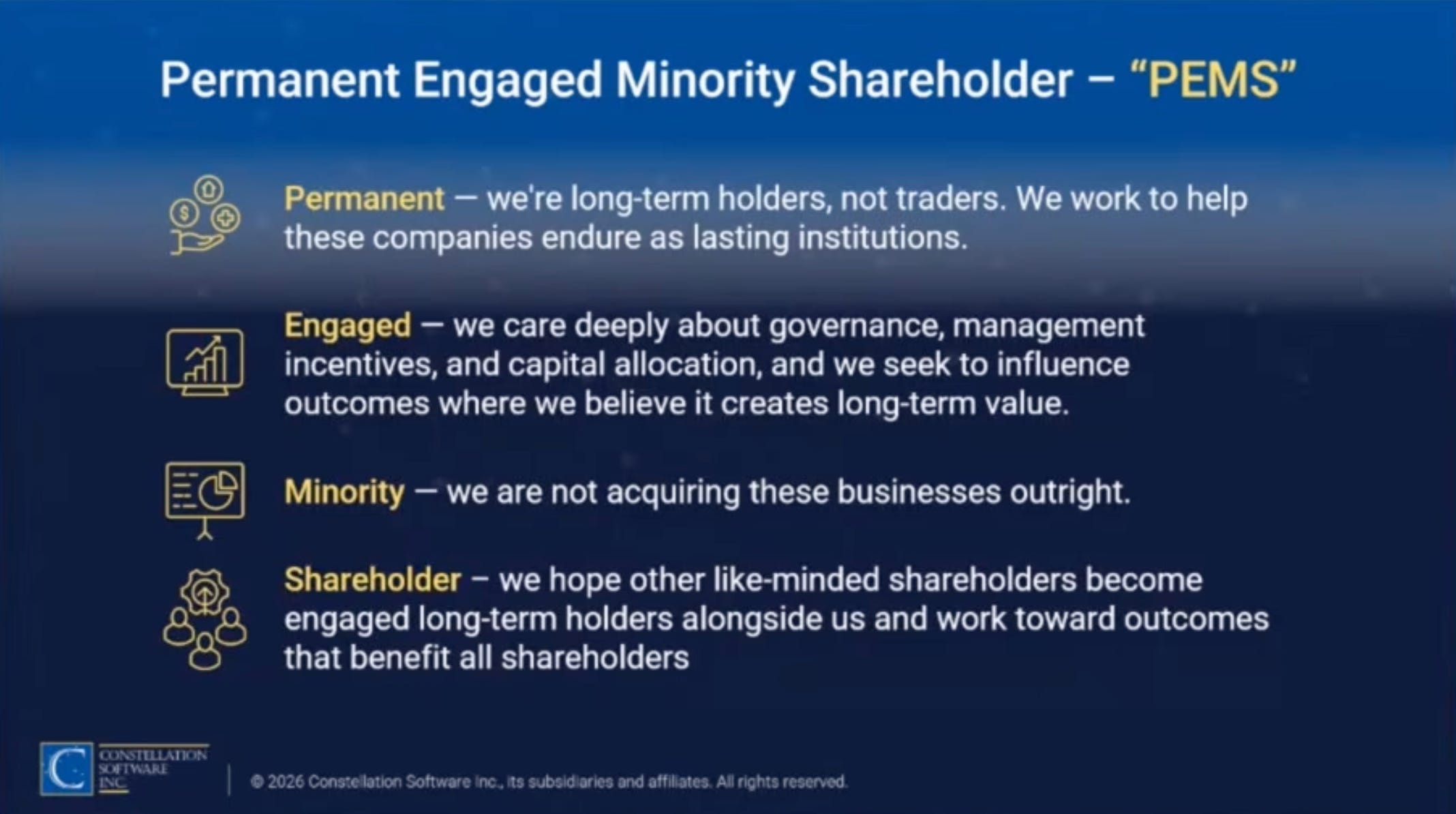

1. PEMS Is the Capital Allocation Playbook for the Next Decade

The most important development in the AGM was the formalization of the Permanent Engaged Minority Shareholder (PEMS) strategy. First Asseco, and now Sabre - the AGM made clear that it is now a core, repeatable part of the playbook.

They can also act like activist investors, improving the underlying operations plus capital allocation decisions, except without the short-termism that plagues most public market activism.

“We’re clearly - we have capital. A lot of people have capital, but we really understand vertical markets, vertical market software businesses… we’re also comfortable buying or being investing in businesses that require some help.” - Mark Miller, President of CSI

CSI is not pitching itself as a passive minority investor; it is positioning itself as an engaged owner that can push existing public-VMS management teams toward the same disciplined capital allocation, share repurchases, and operational rigor that built Constellation.

Bernie Anzarouth (CIO) reinforced the edge:

“Our deep expertise in software - we’ve been at it for over 30 years… We thought a lot about compensation, about investing incremental capital intelligently, and measuring those things, and we think those are useful for people who care about these businesses over the long run.” - Bernie Anzarouth, CIO of CSI

There are two key takeaways from this. First, the price discipline remains intact - management explicitly stated they still prefer acquiring FCF-generating assets over buying back their own stock at current valuations. This means the internal hurdle rate has not been bent to accommodate scale.

Second, the PEMS strategy expands the addressable universe of capital deployment well beyond CSI’s traditional deal flow. The PEMS strategy sidesteps the structural problem we flagged in March - the law of large numbers. As the cash pile becomes larger, it’s harder and harder to put that capital to work.

Because the PEMS strategy lets CSI buy meaningful stakes in undervalued public VMS companies, they are expanding the universe of capital deployment, as they are no longer limited to small private companies. Although the deployment problem still exists, the took-kit to manage the problem has greatly expanded.

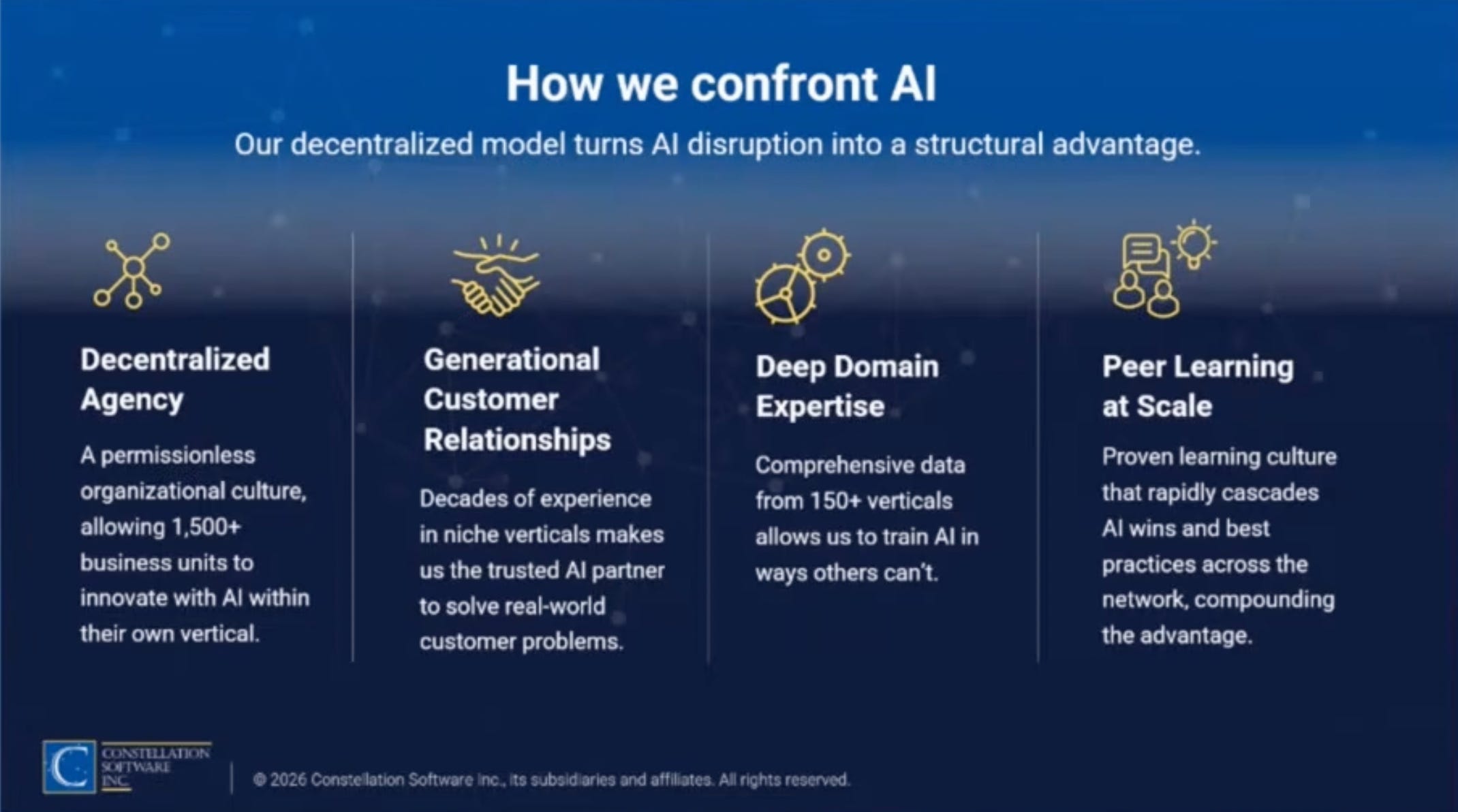

2. AI Is a Tail-Wind

Over the last 12 months the AI panic rippling through all public software names has knocked CSI down 50% peak-to-trough.

“We’ve gone from software eating the world to a fear that AI is going to eat software.” - Jeff Bender, CEO Harris Operating Group

So, how is AI impacting CSI’s business?

“If you think of a cycle time from concept through to production software, typically for us that was measured in months… And as we went through last year, we turned that into days. And today our cycle time is measured in hours.” - David Nyland, CEO Lumine

AI inside Constellation is not being used to slash headcount or compress margins. It is being used to compress development cycle times, meeting customer needs faster than ever.

CSI’s vertical software businesses already own the customer relationship, data, workflows, and distribution in mission-critical software. AI enhances - not weakens - these dynamics, which means more feature delivery, more cross-sell, more pricing power, and a deeper integration into the customer’s workflow.

When asked directly whether AI was driving attrition in any CSI business, Mark Miller’s answer was unambiguous:

“We really haven’t seen any AI-specific attrition… at any point.”

Jamal Baksh (CFO) confirmed this from the data side - he reviews organic-growth trends, and the operational reality being reported is the opposite of the market’s SaaSmageddon narrative.

“I look at about 900 of the businesses, and I look at trending of organic growth, and I follow up with the operating group CFOs, etc., if there's anything that looks like an anomaly - and there are a couple things that might have popped out, and both of them had nothing to do with AI." - Jamal Baksh, CFO of CSI

For a long-term holder, this matters. VMS is a walled garden, and AI deployed within this walled garden creates value for both the customer and the company. The business is being reinforced by AI, not eroded by it.

3. Decentralization is the Secret Sauce

If there was one theme Mark Miller returned to obsessively, it was that Constellation refuses to be run from the center. The decentralization is a protective factor that transcends any specific President or CEO, and the AGM confirmed that management understands the structural reason it matters.

“There’s no CIO who decides what AI platform we use or what we should do or whether we should turn right or left or do this or that. That’s done by our business leaders across the world.” - Mark Miller, President of CSI

And later, even more directly:

“I don’t believe in one corporate culture. We believe in a culture of cultures.” - Mark Miller, President of CSI

Further, decentralization is the single most important reason the company can absorb technological change without breaking. Essentially, the independent business units - who are closest to the customer - can run experiments with technological transitions.

This matters because when the right answer to a given technology shift is genuinely unknowable in advance - as it is with AI - the company that runs the most diverse experiments the cheapest is the company most likely to find the winning play and propagate it horizontally.

It is worth pointing out that CSI has been doing this for three decades. Despite the current noise around AI, the reality is that, within CSI, this is just another instance of machine doing what it has always done.

“We’ve gone through multiple technology changes, and it isn’t because we’ve had a directive from Constellation headquarters as to what to do. Our business leaders decided how to deal with that situation.” - Mark Miller, President and COO of CSI

Mental Model: Bullets, then Cannonballs (from Great by Choice - Jim Collins)

Imagine a ship at sea with a limited supply of gunpowder and ammunition. That ship is approaching an enemy. The ship has two choices - fire bullets or cannonballs. If the ship commits to firing a large, expensive cannonball first, then it commits to spending a substantial amount of resources upfront. If that cannonball misses, then it’s left in a weakened position with less resources.

Instead, if the ship fires small, inexpensive bullets first to gauge wind, distance, and direction, it can commit a small amount of resources, get feedback onto the best approach moving forward, and then use its gunpowder to fire a decisive cannonball.

CSI’s decentralized approach allows the operating businesses to fire bullets, allowing ongoing, low-stakes, continuous experimentation that ultimately drives innovation and strengthens the business over time.

There is no top-down “AI strategy,” coming from the C suite. No strategy directive to force-march the business units onto a standardized platform. CSI is, and has always done, the opposite.

The implications are profound. Firstly, it allows them to respond in real time to any technological change, without taking any new or additional approach. There’s significant antifragility within this model.

Second, the ongoing continuous low-stakes experimentation leads to spawning - the creation of new businesses through low-stakes trial and error. The ever expanding universe of operating groups - including the creation of Andromeda in 2025 - plus the spinoffs of Topicus (2021) and Lumine (2023) are examples of this.

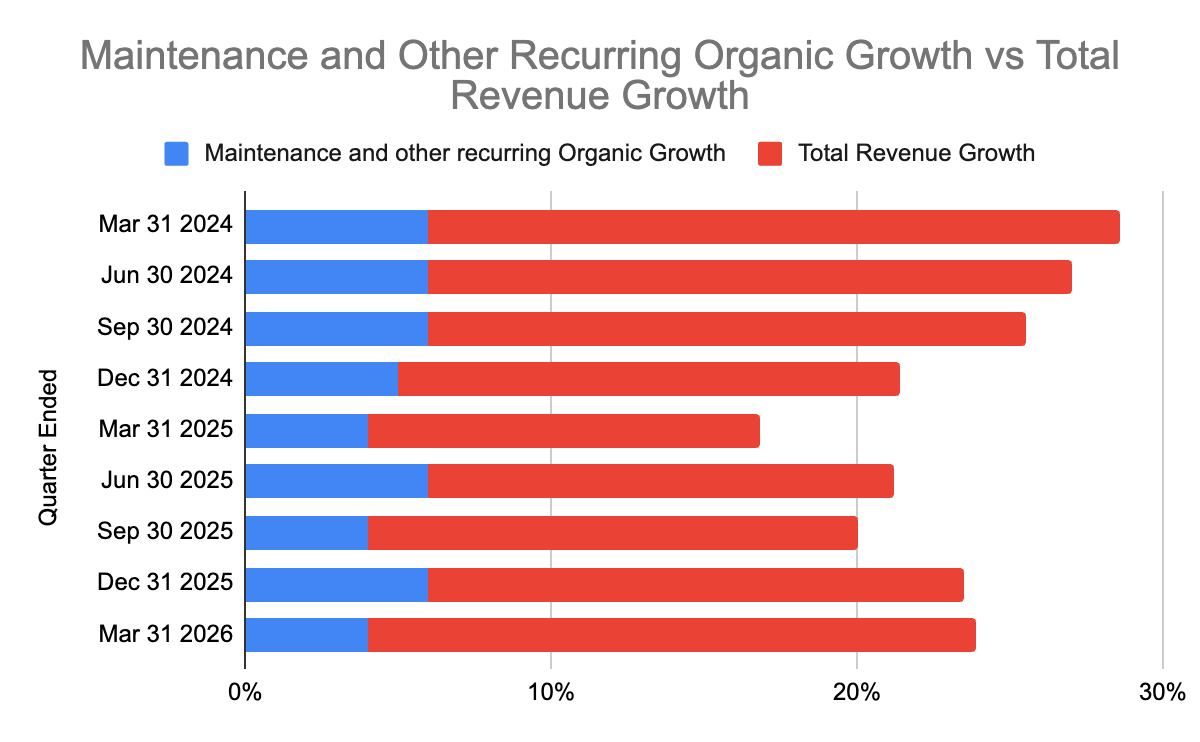

4. A Focus on Organic Growth

The least-headline-grabbing portion of the AGM was also the most strategically interesting: the verticalization panel led by Damian McKay (CEO of Vela Software), with Santina Allen (President, Healthcare Group at Harris Computer), David Nyland (CEO of Lumine), and Bill Delaney (CEO of Modaxo).

The panel’s purpose was to demonstrate how CSI’s portfolio of decentralized business units is being deliberately organized into vertical clusters that produce organic - not just acquired - growth.

Historically, CSI has never been known for strong organic growth.

Mark Leonard has been candid about why.

"Growing organically while generating a high ROIC is, to my mind, the toughest task in the software business" - Mark Leonard, 2013 President's Letter

And in the 2015 letter, he noted the resulting capital-allocation reality:

“We deployed far more (>90%) of our FCF on acquisitions during the last decade, … we care about IRR, irrespective of whether it is associated with high or low organic growth" - Mark Leonard, 2015 President's Letter

Despite what Leonard described in that same letter as a "natural bias towards organic growth" on the senior team, the hurdle-rate discipline - what he calls "magnetic hurdle rates" - has kept “Initiatives” (organic growth) subordinated to acquisitions whenever the latter has cleared the bar.

The 2026 AGM's discussion around verticalization is meaningful in that context: not as a pivot away from acquisitions, but as the first credible mechanism CSI has produced for inflecting the organic growth line without compromising the IRR discipline.

Santina Allen made the clearest case. Harris’s healthcare portfolio now spans the entire patient journey - acute hospital systems, physician practice systems, specialty solutions, retail and independent pharmacies, radiology, long-term care, and payer-side platforms (including, she noted, the leading Medicare shopping and enrolment platform serving 60M+ members).

“Collaboration of those businesses gives us opportunities to learn about the unique space, the demands, the regulatory environment… Lots of different benefits from that ecosystem that we serve.” - Santina Allen, President, Healthcare Group at Harris Computer

She specifically called out cross-selling within the vertical as one of the measurable outputs of that collaboration.

Interestingly, in the Q&A section management talked about tinkering with management compensation to specifically incentivize organic growth, although they emphasized this is still experimental and in it’s early stages.

Regardless, operationally, CSI has two organic-growth levers operating simultaneously: AI enabled engineering throughput against an enlarged feature backlog, and tighter integration with customers whose specific needs can be met through multiple sibling business units.

The maintenance and other recurring line has a credible path to inflect upward if even a portion of this verticalization-plus-AI machinery works as designed.

5. The Aperture Is Widening

The final theme from the AGM is that Constellation is willing to expand its acquisition aperture beyond pure VMS - but only where the ROIC math holds. Three specific moves stood out.

VMS Ventures is incubating AI-native startups internally, including the deployment of AI agents through the “Rhea” initiative. The goal is to seed the next generation of operating businesses rather than buy them at higher prices later.

Hardware and tech-enabled services were explicitly acknowledged as areas where CSI is comfortable acquiring, provided the defensive characteristics resemble those of VMS.

Horizontal software remains a viable target as long as it carries deep defensive characteristics within a specific geography or niche.

This is an important point worth repeating: CSI prizing internal hurdle rates over the VMS business model specifically. Said another way, investors shouldn’t view CSI as a VMS acquirer; instead they should view it as an investment vehicle.

The unifying constraint is the ROIC threshold, not the industry vertical. As long as the discipline holds, the universe of acquirable assets expands materially.

The risk here, of course, is style drift. Although the aperture is widening, the real test will be whether the discipline that produced the historical ~35% CAGR survives that expansion.

Mark Miller’s framing was characteristically tight:

“It’s who you are, not who you say you are. It’s what you do, not what you say you’re going to do.” - Mark Miller, President of CSI

We read this as a commitment to internal continuity, regardless of how the capital is deployed.

The Verdict

In March, we wrote that:

“the protective factors that have led to exceptional capital allocation historically — disciplined capital allocation, decentralized structure and aligned incentives — remain in place.”

The 2026 AGM further demonstrated that management understands precisely why those factors are protective, and has built the next leg of the strategy around preserving them while expanding the deployment toolkit.

The PEMS playbook is a credible answer to the law-of-large-numbers problem. Decentralization will allow the organization to adapt to and utilize AI. Verticalization plus AI-compressed cycle times provide a credible answer to the organic-growth question. Finally, the cultural architecture that makes all three possible, the culture of cultures, is being deliberately defended by management.

We think the central thesis is unchanged - CSI’s long-run success hinges entirely on management’s ability to resist overpaying for growth while continuing to manage a decentralized organization. This is as it has always been.

Our friend, Substacker, and fellow CSU shareholder The Compounding Tortoise sums it up best:

”Despite all the noise in the market, surprisingly little has changed.”

Enjoy what you read?

Continue the pursuit! Browse our full archive of posts below 👇

Disclaimer: We are private investors and not financial advisors. This post is for educational purposes only and does not constitute financial advice. Constellation Software Incorporated (CSU) is a stock we currently own. Always conduct your own due diligence before making any investment decisions.