lululemon athletica: Mismanaged Compounder, or Value Trap?

Fighting for relevance while navigating a boardroom battle for the soul of the company

Over the last 18 months lululemon athletica inc. (LULU) has been a perpetual (downward) dog. For shareholders, the ride has been anything but a smooth vinyasa flow.

The shares has been nearly halved from their highs, battered by a perfect storm of slowing U.S. consumer spending, execution missteps, boardroom battles, and the rise of “cooler” competitors like Alo Yoga and Vuori.

The prevailing narrative on Wall Street is one of saturation and decline, fuelled by decelerating sales in the Americas and the optics of a leadership vacuum following the recent departure of CEO Calvin McDonald.

However, looking at the underlying business, we see something entirely different. We see a company generating a 39% Return on Invested Capital (ROIC). We see a balance sheet with $1 billion in cash and zero debt. You see a business growing revenue at 46% in China.

This disconnect between price and fundamentals is the playground of the activist investor. Enter Elliott Management.

In late 2025, Elliott disclosed a stake exceeding $1 billion in lululemon. Elliott is not a passive tourist; they are arguably the most effective operational activist in the world. Their recent campaigns at Starbucks (replacing the CEO with Brian Niccol) and Southwest Airlines demonstrate a playbook focused on restoring operational rigor to drifting giants.

For the long-only equity investor, the current setup presents an asymmetry - a market valuation that prices the equity as a permanently impaired asset, juxtaposed against a business model that retains one of the highest returns on invested capital (ROIC) in the consumer discretionary sector.

Is lululemon a dying brand, eroding before the market’s eyes under increasing competition? Or is it a mismanaged compounder ripe for operational optimization?

To answer this question we’ll dissect the business, break apart the financial statements, look at it through our Four Pillars of Quality, do a five year discounted cash flow, get a second opinion with ValuationBot.AI, and come to a final verdict.

Let’s dive in.

Table of Contents

Pillar 2: The Moat

Pillar 3: Return on Invested Capital (ROIC) and Return on Incremental Invested Capital (ROIIC)

The Business

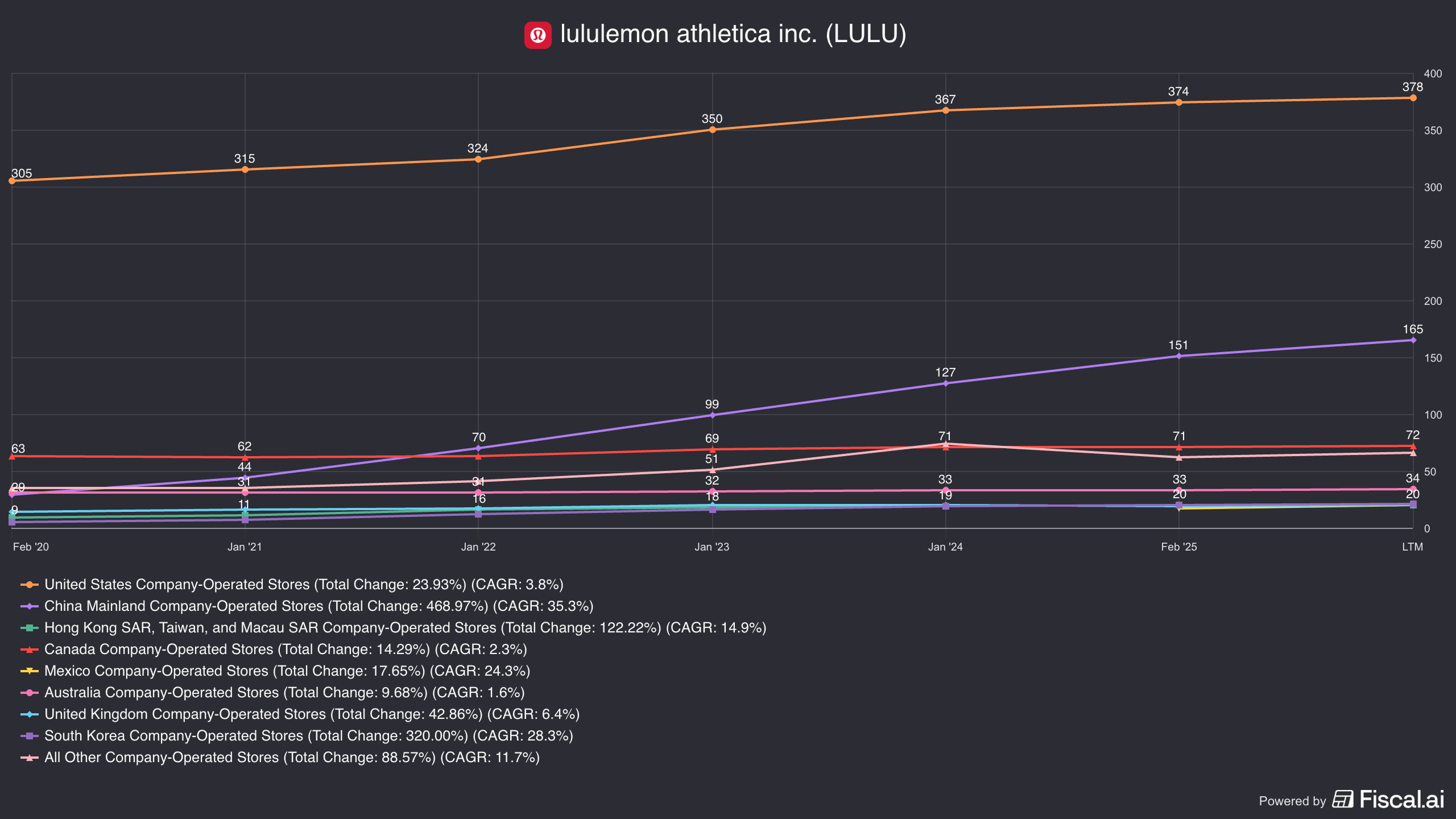

Lululemon athletica inc. (LULU) is currently a $24.5 billion market cap company that is a vertically integrated technical apparel retailer. Unlike Nike or Adidas, which rely heavily on wholesale partners (Foot Locker, Dick’s Sporting Goods), lululemon sells almost exclusively through its own channels—its 796 company-operated stores and its website.

For nearly two decades, lululemon enjoyed a blue ocean in the athleisure market, defining the category and enjoying pricing power akin to a luxury house. That era has ended.

The competitive landscape has shifted to a red ocean characterized by increasing competition, specialized insurgents targeting specific demographics, and a dupe culture that undermines lululemon’s technical innovations.

The company operates under the “Power of Three x2” strategic framework, unveiled in 2022. The goal is to reach $12.5 billion in revenue by 2026 by hitting three specific targets relative to 2021 levels:

Double Men’s Revenue: Moving beyond the yoga studio to capture the male functional apparel market.

Double Digital Revenue: Leveraging their e-commerce ecosystem.

Quadruple International Revenue: Exporting the brand beyond North America.

While the North American cylinder of this engine is currently misfiring, the international cylinder is running hotter than expected. lululemon is no longer just a North American yoga brand; it is becoming a global wellness lifestyle house.

The Insurgents: Alo Yoga and Vuori

In North America, lululemon is currently fighting a two-front war. On one flank is Alo Yoga, attacking the fashion-forward female demographic; on the other is Vuori, besieging the male demographic.

Alo Yoga: The Battle for “Cool”

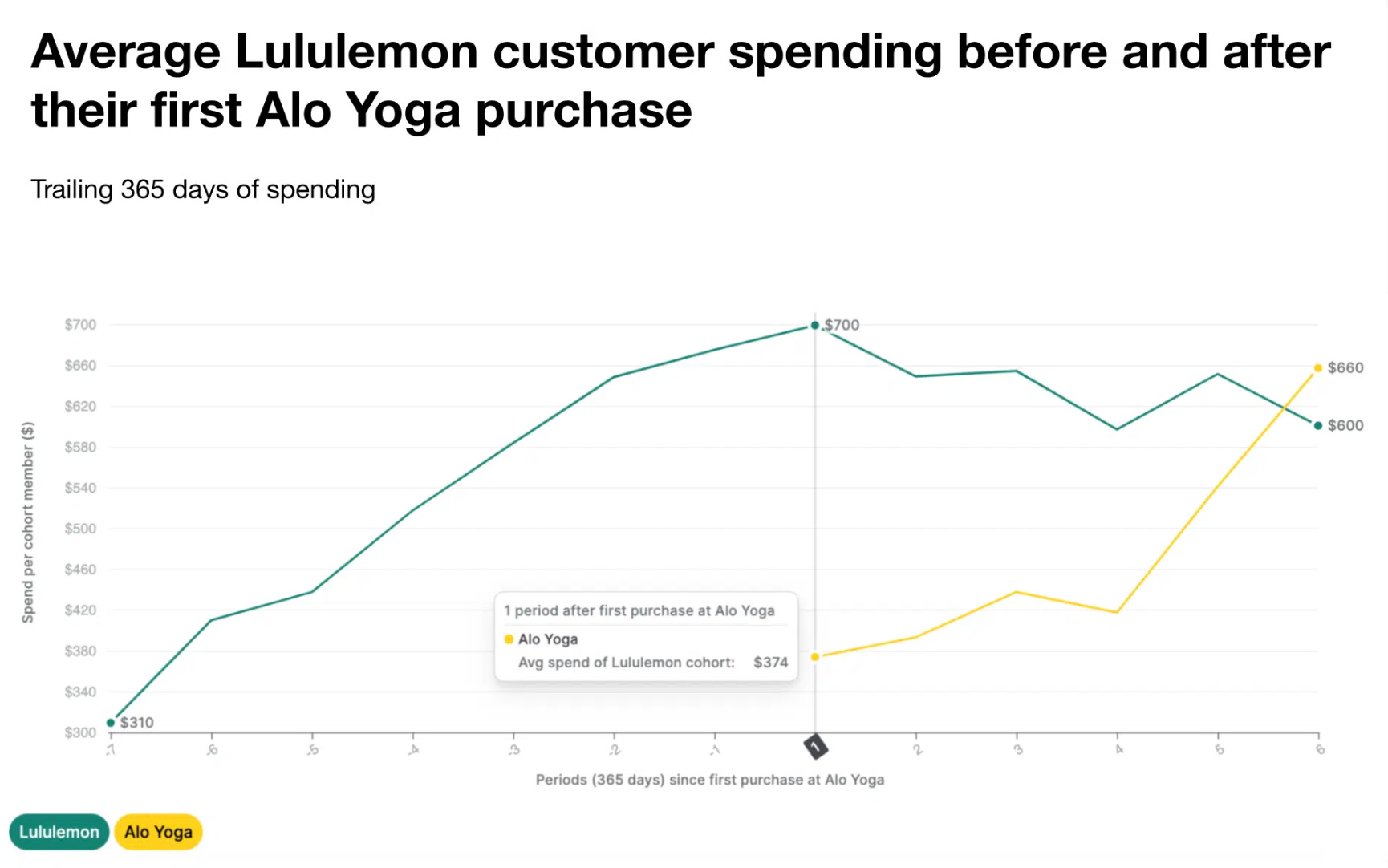

Alo Yoga has successfully positioned itself as the “it” brand for the Gen Z and young Millennial consumer. Unlike lululemon, whose brand ethos is rooted in “sweat” and performance, Alo positions itself as a “studio-to-street” fashion label. This distinction is subtle but critical. Alo’s marketing, heavily reliant on high-profile influencers like Kendall Jenner and Hailey Bieber, creates a halo of exclusivity and trendiness that lululemon - now ubiquitous in suburban shopping malls - struggles to match.

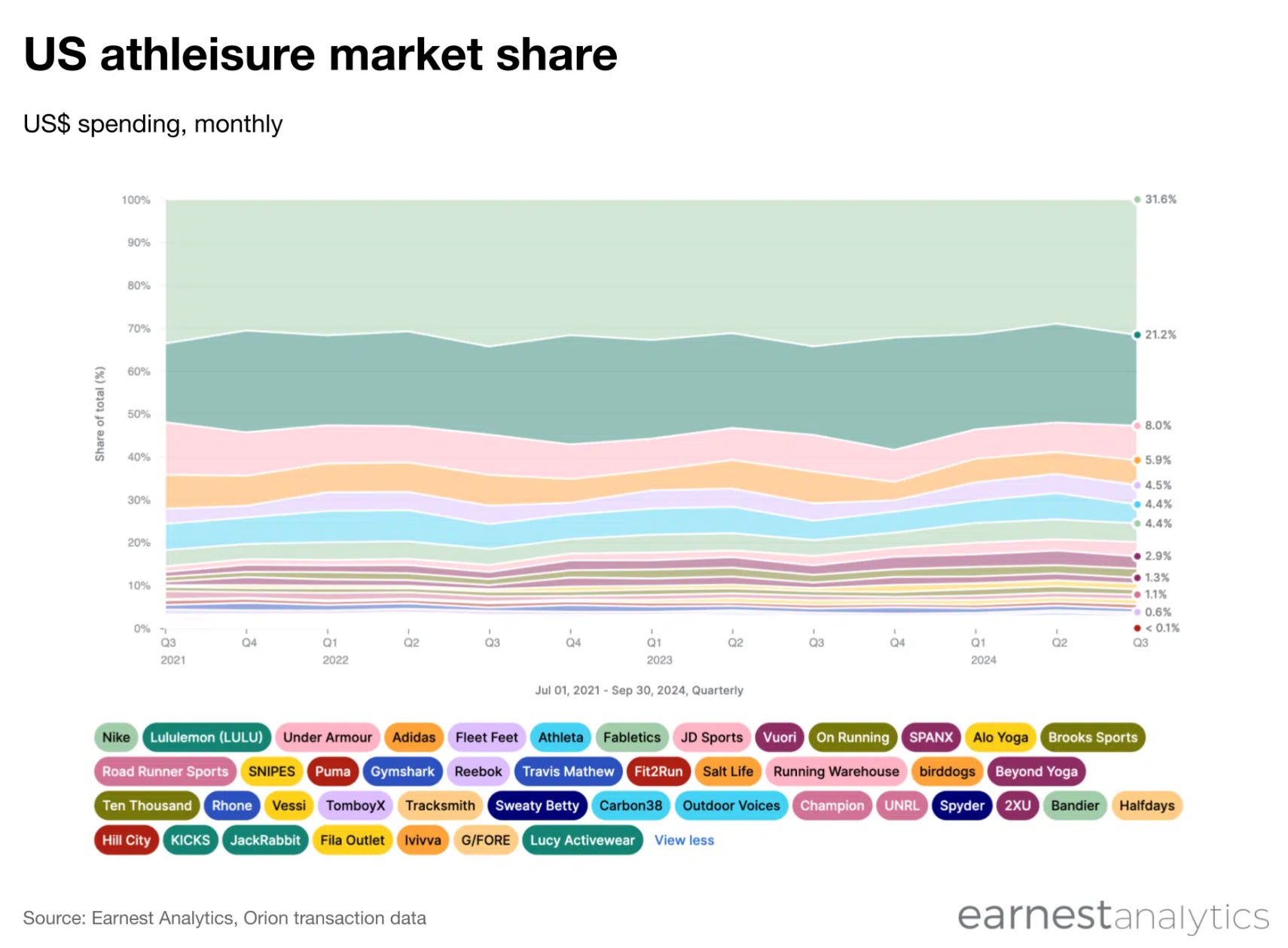

Data from Earnest Analytics indicates that while lululemon retains a dominant 21.2% share of the U.S. athleisure market, Alo is growing rapidly from a smaller base of 1.3%. Alo’s retail strategy, focusing on “sanctuary” stores in high-visibility urban centers, mirrors lululemon’s early playbook but with a higher fashion quotient. By expanding into categories like luxury handbags and wellness, Alo is capturing the “lifestyle” spend that lululemon covets.

For lululemon, the risk is not just lost sales, but a loss of relevance. In fashion, relevance is a leading indicator of pricing power; if lululemon becomes seen as the “safe” or “older” choice, its ability to command $128 for leggings diminishes.

Vuori: The Threat to the Men’s Growth Pillar

The “Power of Three x2” strategy relies heavily on doubling the men’s business. While also having a women’s line, Vuori is attacking lululemon's men’s business. Vuori identified a gap in the market that lululemon missed: men who want high-quality activewear but feel alienated by lululemon’s technical, slightly feminine brand heritage. Vuori’s aesthetic - ”California Coastal” - is softer, more relaxed, and explicitly masculine without being aggressive.

Vuori’s recent $825 million capital injection, valuing the company at $5.5 billion, provides it with the war chest to scale its retail footprint to 100+ stores by 2026. Crucially, Vuori boasts a higher Net Promoter Score (NPS) for fit and comfort than lululemon.

Lululemon’s “ABC” franchise (Anti-Ball Crushing) was a massive hit, but innovation in the men’s category has stagnated. Vuori is capitalizing on this stagnation, and its rapid retail expansion means it will increasingly be co-located with lululemon in prime malls, offering a direct alternative to the male shopper.

The Incumbent: Nike’s Stumble and Opportunity

Nike remains the market leader with over 31% share, but it is currently a wounded giant.

Nike’s strategic misstep - cutting wholesale partners to focus on DTC, only to lose shelf space to Hoka and On Running - has forced it into a defensive posture.

Nike is now aggressively discounting to clear inventory and regain market share. This promotional intensity from the market leader puts pressure on the entire sector’s pricing architecture. If Nike is discounting premium leggings to $60, lululemon’s $98 price point faces greater resistance from the marginal consumer.

The “Dupe” Culture: Commoditization of Innovation

Perhaps the most insidious threat to lululemon’s moat is Dupe Culture. Driven by TikTok and Instagram Reels, consumers are increasingly seeking low-cost alternatives that mimic the look and feel of lululemon products. Retailers like Costco, Amazon, and SHEIN offer “dupes” for as little as $20-$30, compared to lululemon’s $98-$128.

According to eMarketer, around one-third of makeup consumers ages 18 to 34 (33%) and 25 to 34 (35%) bought a dupe due to something they saw on social media. And research conducted by Alexandra J. Roberts for Northeastern University’s School of Law, revealed that “71% of Gen Z and 67% of Millennials report they sometimes or always buy dupes. Where older generations clandestinely purchased dupes hoping to pass them off as the real thing, young bargain-hunters eschew gatekeeping and proudly share their finds with friends and followers.” - How Dupe Culture is Reshaping Retail

Lululemon has responded aggressively, trademarking “LULULEMON DUPE” to control search advertising and filing lawsuits against Costco for trade dress infringement.

The existence of high-quality dupes is a huge threat to lululemon - if the consumer cannot feel the difference between a $30 legging and a $100 legging, this means lululemon is differentiated only by intangible brand equity rather than tangible product superiority - precisely at a time when that equity is under attack.

Unforced Errors

In a distinct echo of the 2013 “Luon” crisis, lululemon paused online sales of its new “Get Low” collection in North America in January 2026. Customers reported that the fabric was sheer (see-through) during squats. While the product remained available in Europe and physical stores, the online pause was a brand and reputational blow, reinforcing the narrative that lululemon’s technical dominance is slipping.

Lululemon also had another product launch failure with its Breezethrough line in 2024, where customers complained about the design, specifically pointing to a V-shaped waistband and a Y-shaped seam in the back that caused a "whale tail" or "long butt" look.

The line was quickly pulled from the shelves after a large and swift consumer backlash. These repeated missteps raise fundamental questions about the consistency of the R&D and innovation, as well as the competency of their quality control.

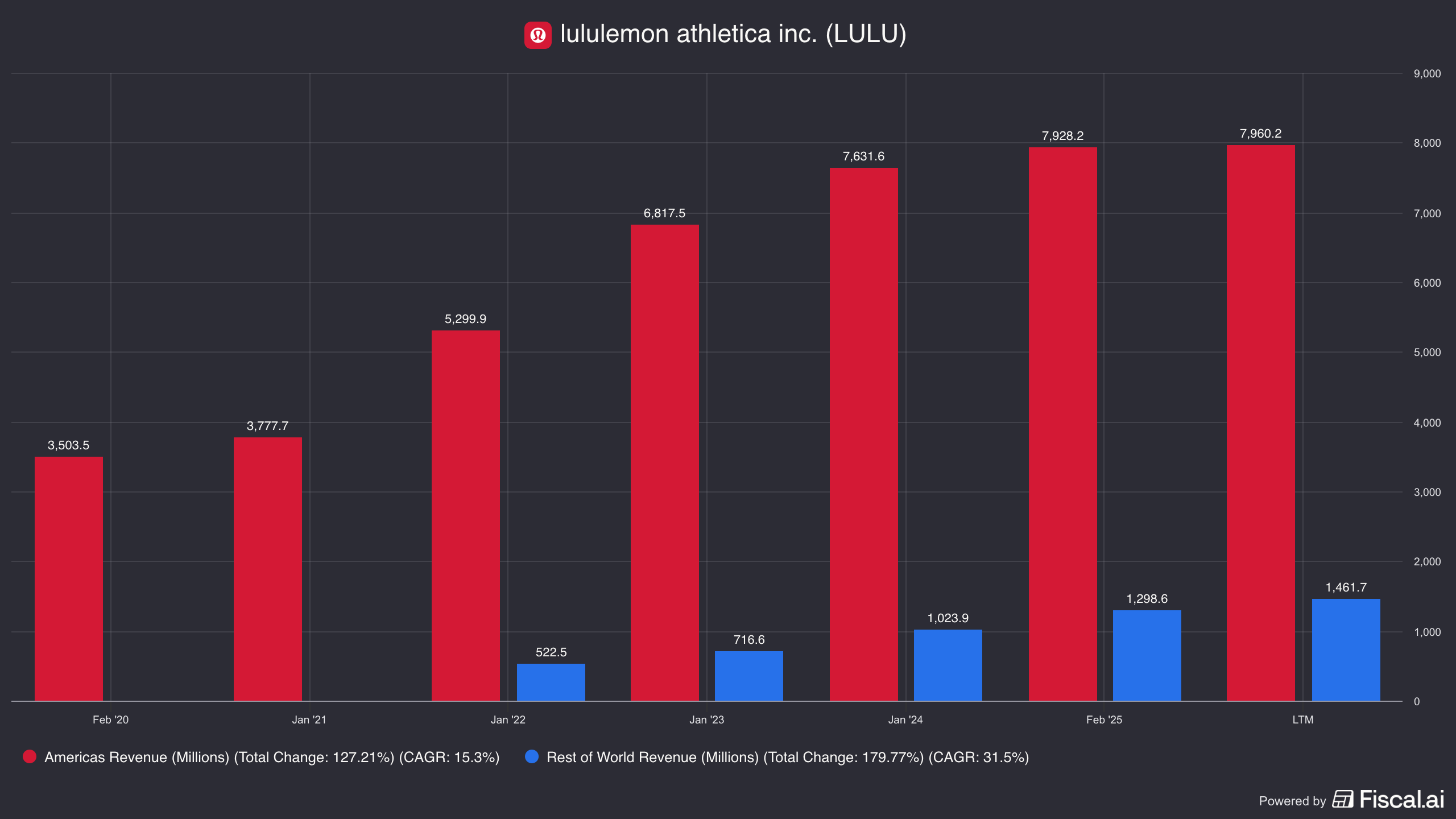

North American Saturation vs. International Acceleration

Historically, lululemon’s exponential growth was based on its dominance in the United States and Canada. However, its growth is now coming from its International business as the North American market is highly saturated and increasingly competitive.

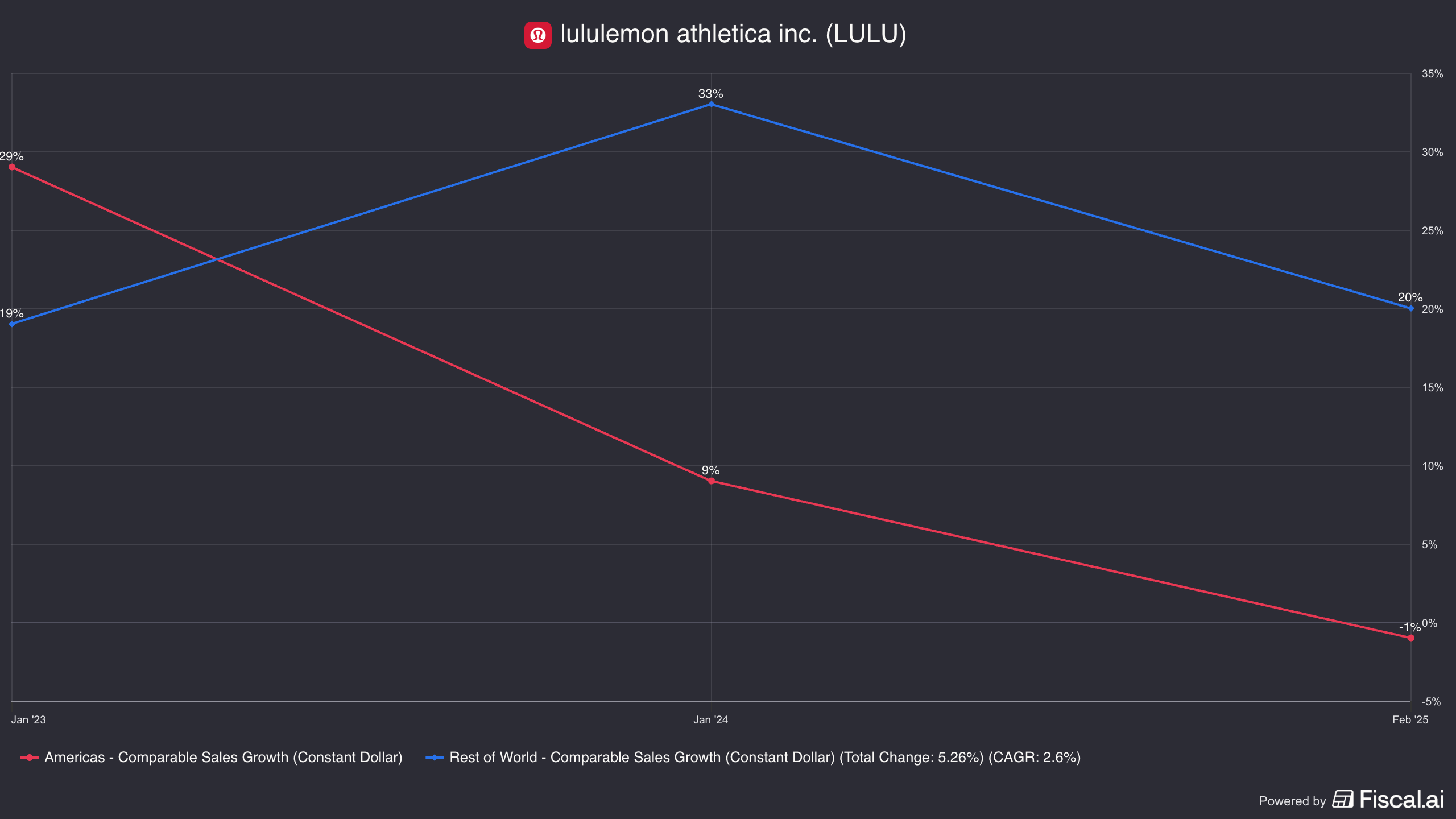

In its most recent quarter, the Americas segment, which still accounts for approximately 68% of total net revenue, experienced a revenue contraction of 2%, with comparable sales declining by 5%. In sharp contrast International net revenue surged by 33% in Q3 2025, with comparable sales increasing by a robust 18%.

This growth was not isolated to a single geography but was broad-based. The “Rest of World” segment reported a revenue increase of 19% (19% on a constant currency basis), reaching $367.2 million for the quarter. This segment now represents approximately 14% of total net revenue.

The divergence has profound implications for capital allocation. The company is actively redirecting resources away from domestic store expansion toward international market penetration.

Although most of their stores are within the United States, lululemon has been aggressively investing in a mainland China expansion, going from zero stores in 2016 to 165 stores nearly a decade later.

The Income Statement: A Tale of Two Geographies

The income statement reveals the impact of the company fighting a two-front war, while also working to aggressively expand internationally.

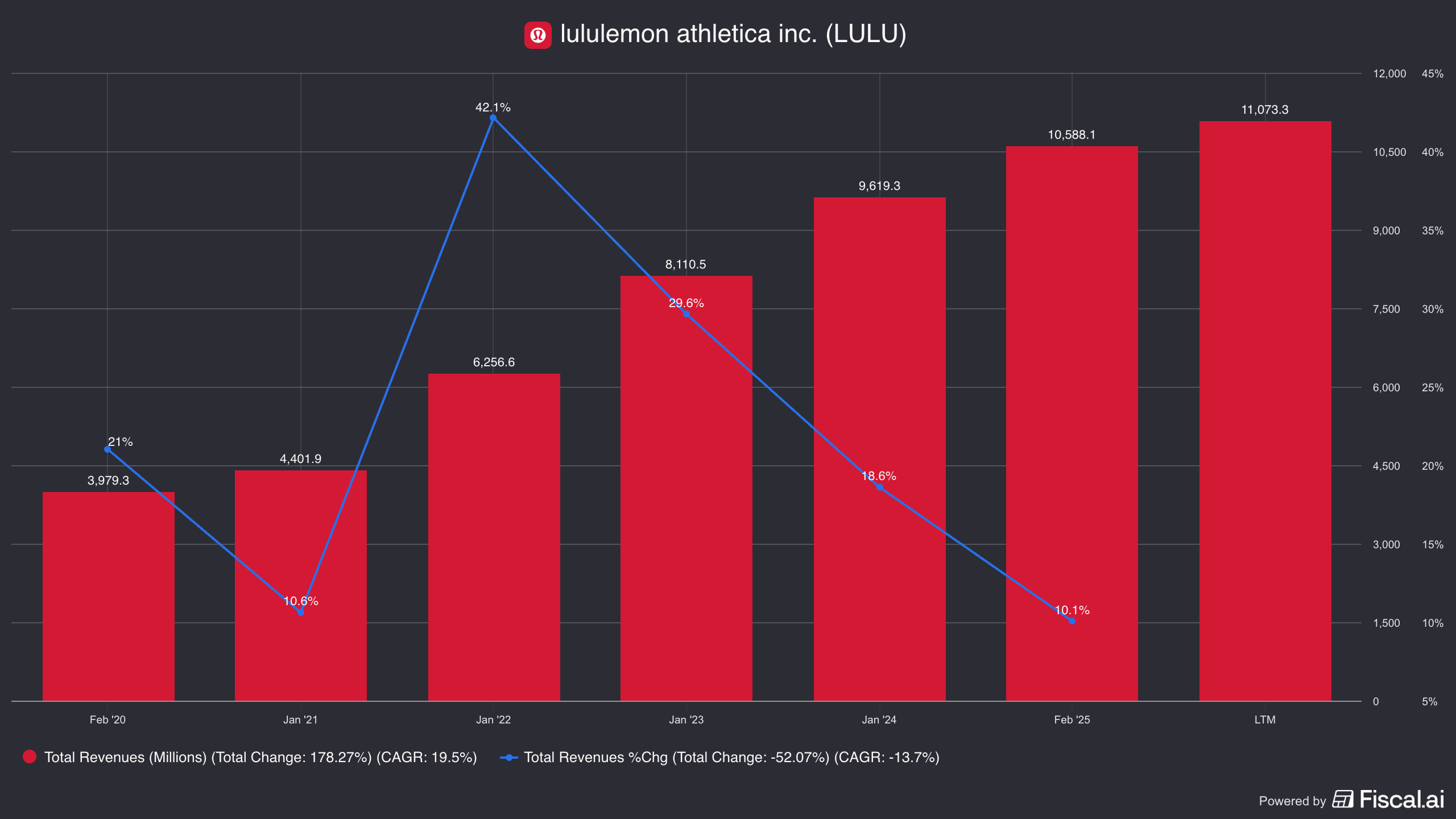

Revenue

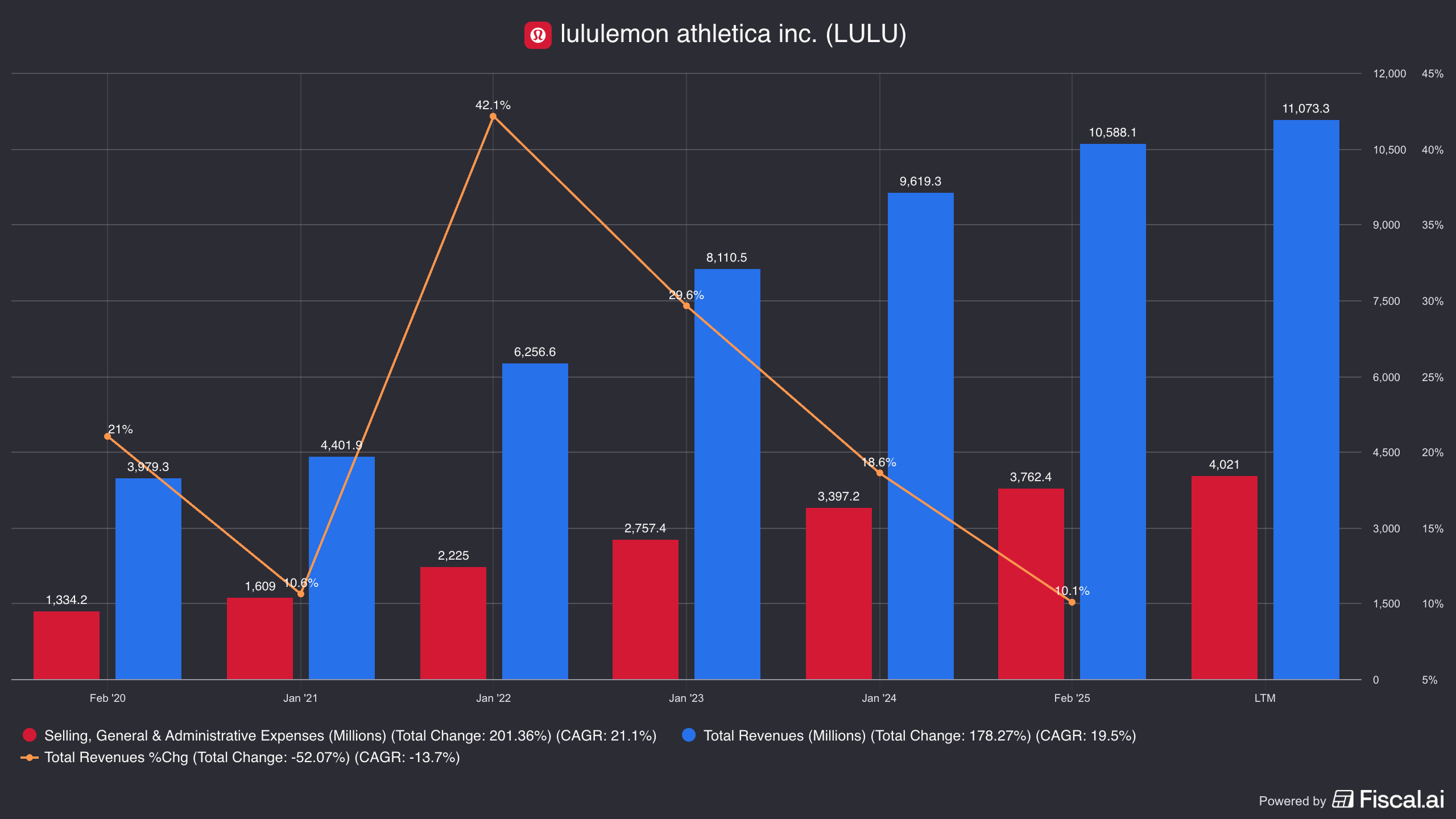

We can see ongoing deceleration in overall revenue growth, which may drop into high single digits for Fiscal 2025.

However, when we break it down into geography, we can see that their International business is booming, while their North American business is stagnating.

We can see as well that same store sales growth is negative in the North American business, while it remains double digit (albeit contracting) in the International segment.

It does appear that the brand is resonating deeply with international consumers, which is a hedge against U.S. maturity.

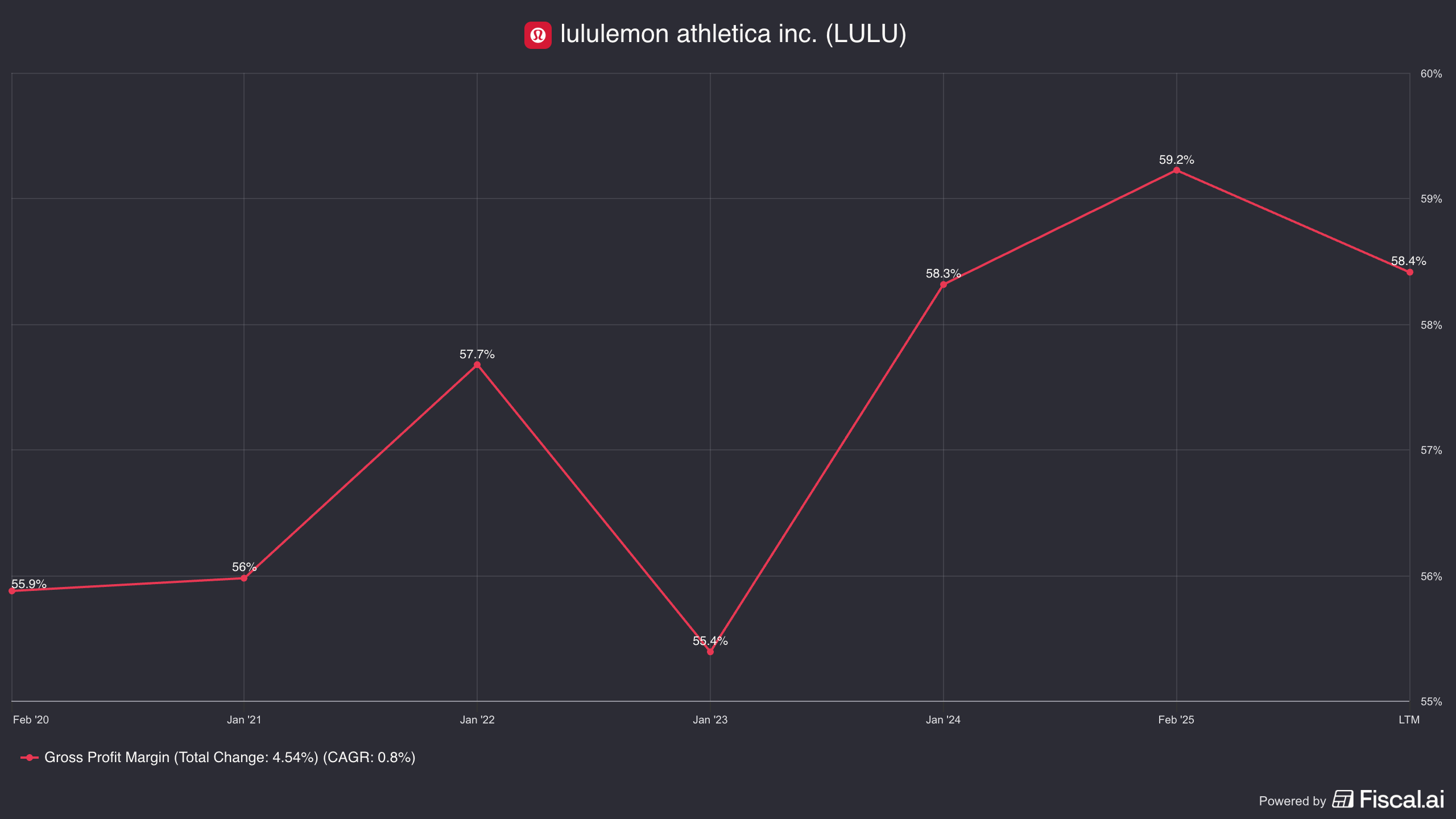

Gross Margin Compression

Gross margin compression is the primary source of the bearish thesis. Gross margin has been drifting down, and it fell 280 basis points to 55.6% in Q3 2025.

Management attributes this to two factors - markdowns and tariffs.

In the North American business, lululemon was forced to discount product to clear slow-moving inventory. For a brand built on pricing power and scarcity, this is a red flag.

Tariffs, hit lululemon twice. Firstly, they source heavily from China and SE Asia which impacts their cost of goods sold (COGS). Secondly, the removal of the U.S. de minimis exception (duty-free for shipments under $800), negatively impacts lululemon's profits by increasing e-commerce fulfillment costs.

SG&A Bloat

Despite the slowing revenue growth, Selling, General, and Administrative expenses continue to rise and, as of Q3 2025, represent 38.5% of revenue. In a period of slowing sales, expenses should ideally be tightening. The fact that SG&A is growing faster than revenue indicates “operational bloat” and is an area that an activist investor can target.

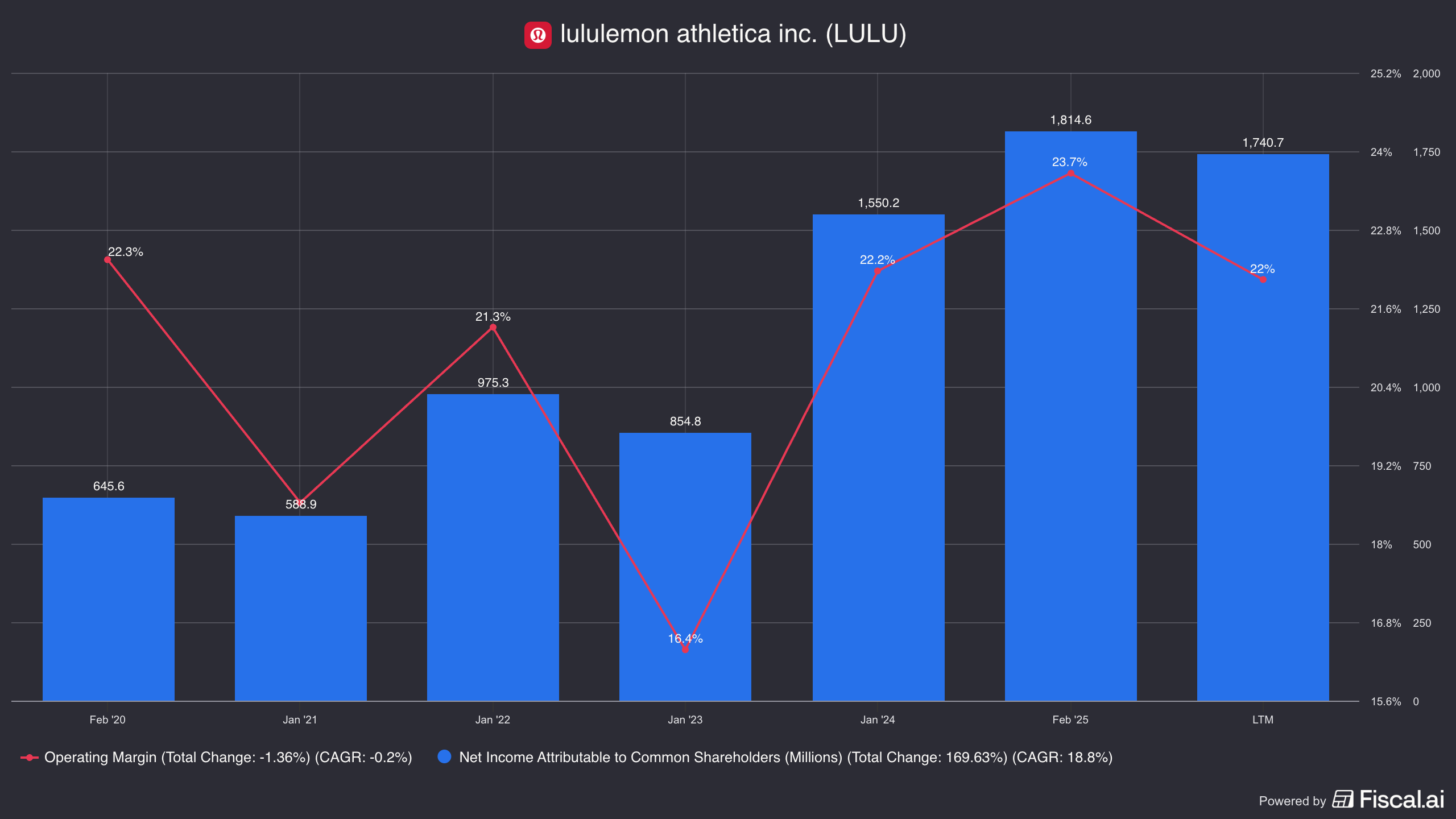

Operating Margin

Adding it all up it’s easy to foresee how lululemon's operating margin (and, thus, profits) are coming under strain. Although historically quite healthy, they dropped to 17% for Q3 2025.

A note about the 2023 operating margin - this was negatively impacted by a non-cash charge booked related to the Mirror acquisition. After adjusting for this, their 2023 operating margin was about 23%. So, dipping below 18% would mark a new low for the company, post pandemic.

The Cash Flow Statement

Despite the challenges, lululemon continues to generate copious amounts of cash.

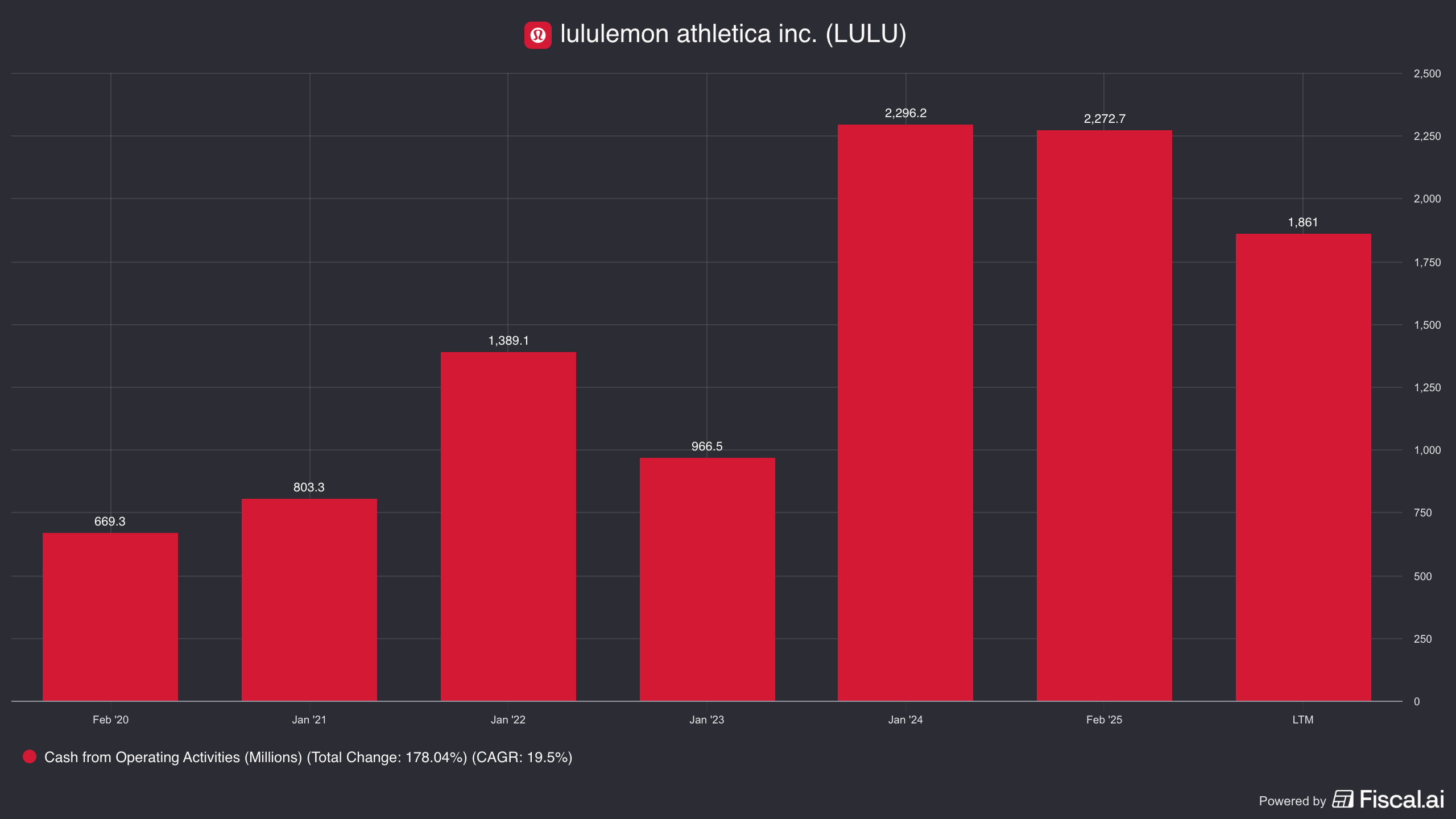

Operating Cash Flow (OCF)

Over the last five years lululemon’s operating cash flow (OCF) has been highly volatile. Much of this relates to the initial supply chain and inventory shocks of the initial pandemic,

Between 2020 and 2025, the volatility in lululemon’s OCF - ranging from $669 million to nearly $2.3 billion- tells the story of a supply chain under siege, with a subsequent recovery. The stability between FY2023 and FY2024 OCF signals a return to a “steady state” operational cadence, where cash generation is driven by organic earnings growth rather than working capital swings. The company demonstrated that its mature business model is a prolific cash generator, capable of producing over $2 billion in liquidity annually.

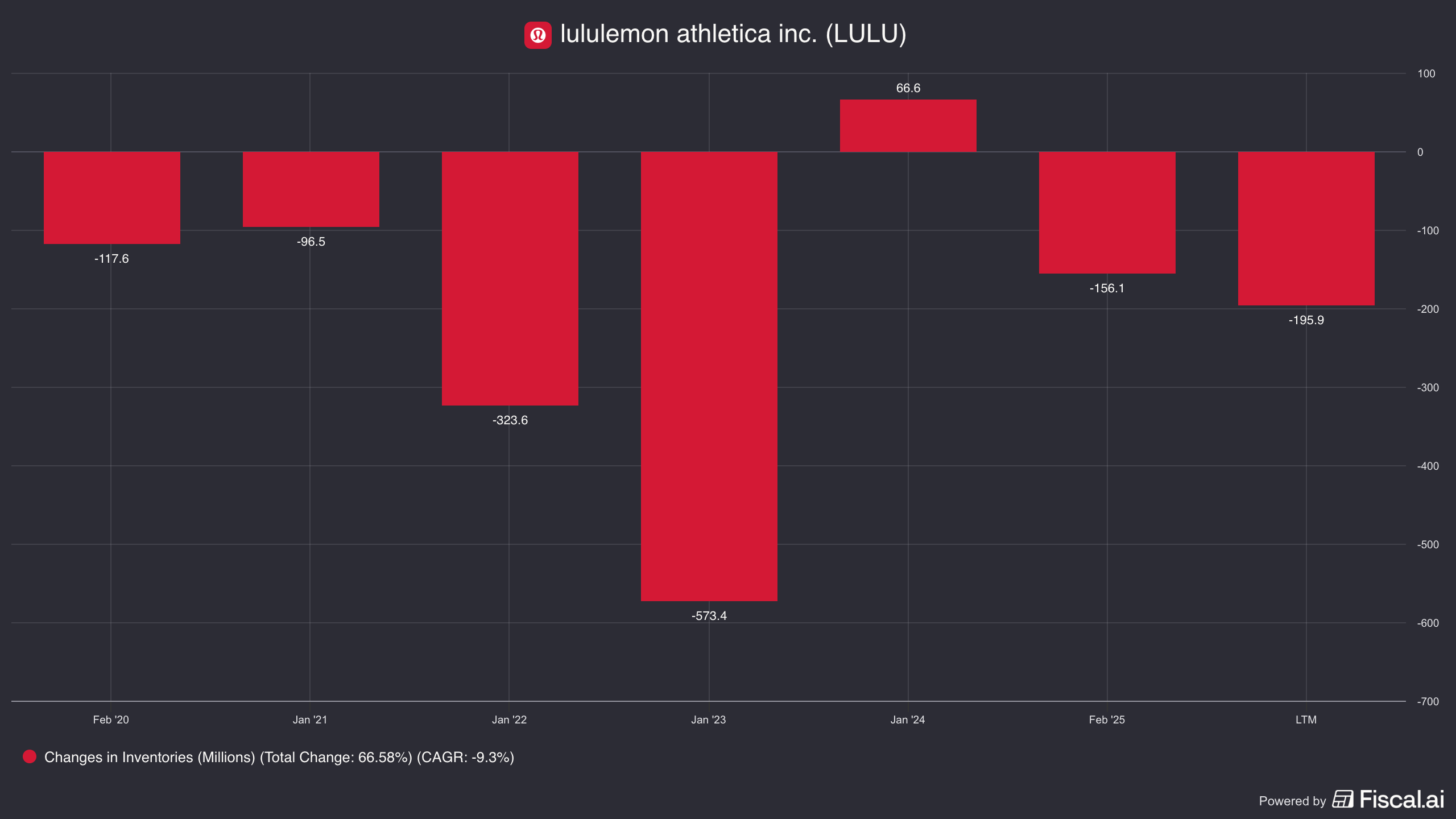

The current headwinds are starting to negatively impact cash generation, as OCF for the most recent quarter (Q3 2025) is down ~12%. In addition to a declining net income, lululemon is also building some inventory in late 2025. This is partially due to declining sales, and partially defensive due to tariffs.

As we can see though, the recent inventory build pales in comparison to the inventory glut the company experienced in 2023, coming out of the supply chain crisis.

Finally, a specific and unusual drag on FY2025 cash flow has been the sharp increase in “Prepaid and Receivable Income Taxes”, which ultimately relates to the timing of certain tax payments. It does impact cash, although it’s due to a timing mismatch that will reverse (inflow) in future quarters, when refunds are processed, or liabilities are offset.

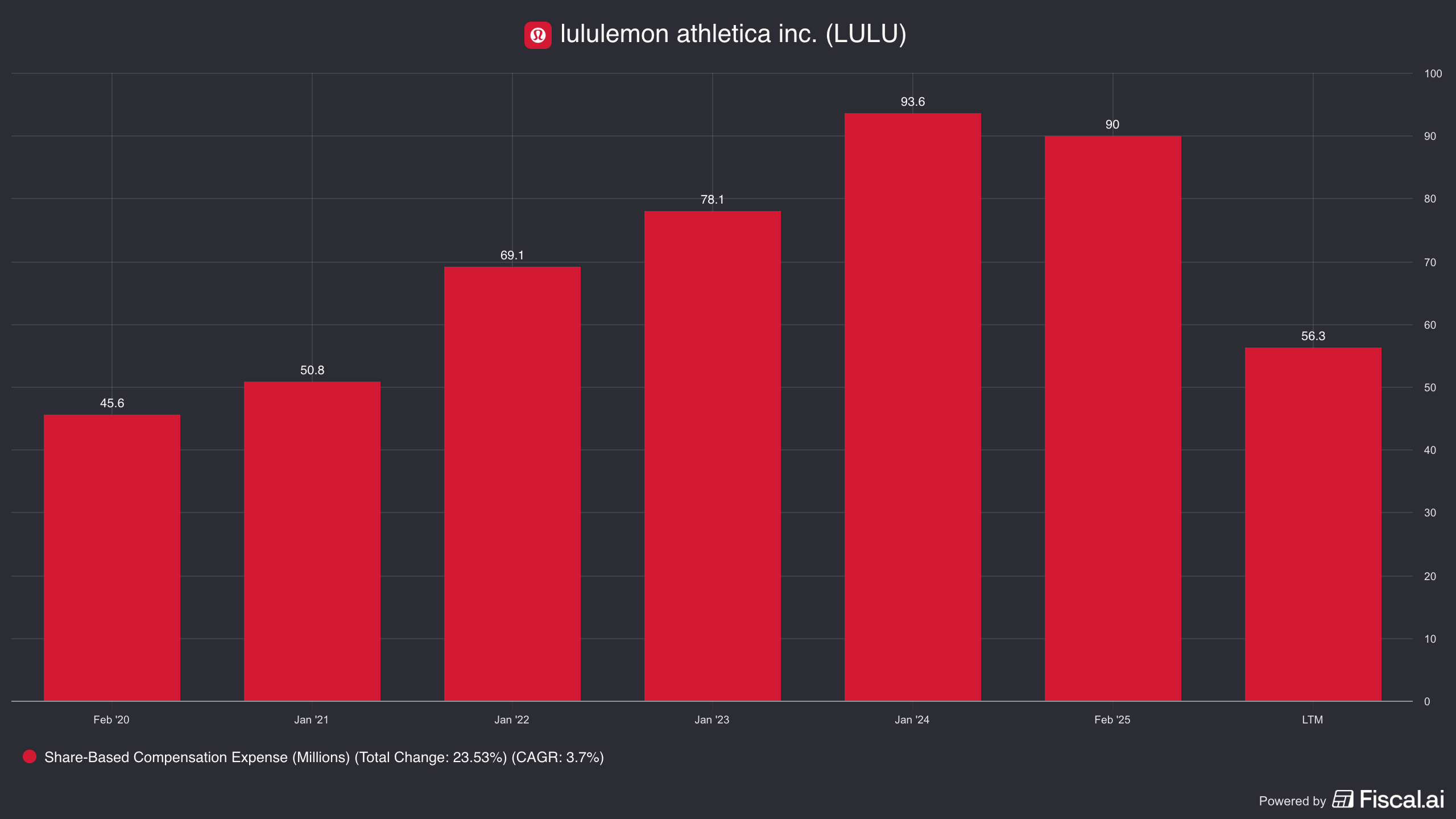

Share Based Compensation (SBC)

Even though SBC is a “non-cash expense” and added back onto the cash flow statement, we believe it is a cost, we generally assess it with the cash flows of the company.

When lululemon executes buybacks to offset the dilution, they consume cash in the Financing section (via buybacks) to prevent share count inflation. The net economic cost to the company (and investors) is real, even if the OCF line item suggests otherwise.

In the post pandemic period we can see SBC has been growing, although it remains overall a very small percentage of operating cash flow (~4%).

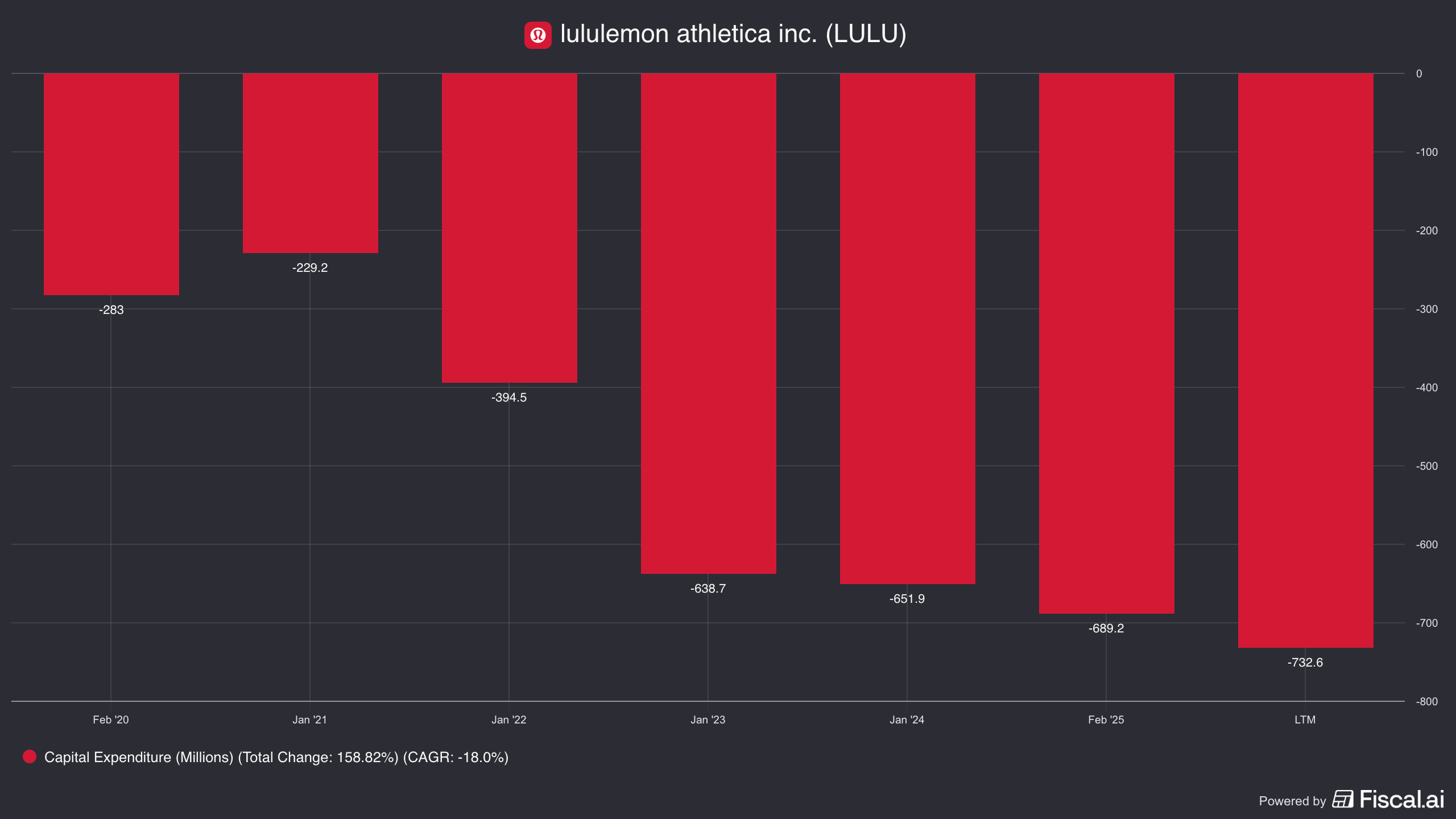

Capital Expenditures (CapEx): Investing in the Omni-Channel Moat

The “Investing Activities” section of the cash flow statement is dominated by Capital Expenditures. For lululemon, CapEx is the fuel for the “Power of Three” strategy, funding the physical stores, digital platforms, and supply chain automation required to double the business.

Building Bricks and Getting Clicks

Usually, retail CapEx is synonymous with new store openings. For lululemon, the narrative is more nuanced. CapEx has scaled from $229 million in FY2020 to $689 million in FY2024.

Despite the digital boom, physical retail remains central. Lululemon opened 56 net new stores in FY2024, ending with 767 locations. However, the nature of these stores has changed.

New locations, particularly in China (Tier 1 cities) and key North American markets, are larger, “experiential” flagship formats. These require higher upfront capital per square foot but generate significantly higher sales per door.

Further, a significant portion of the annual CapEx budget is allocated to technology. This includes the migration of ERP systems to the cloud, the enhancement of the mobile app (which drives nearly 50% of revenue), and data analytics platforms for personalized marketing. The snippets reference “technology investments” consistently alongside store capital.

M&A Activity: The MIRROR and Mexico

In the last five years lululemon has undertaken some M&A activity, with mixed results.

In FY2020 lululemon spent $500 million on the acquisition of MIRROR (home fitness hardware) in FY2020. This was a terrible move and has undoubtedly destroyed value. Lululemon has taken impairments on the majority of the acquisition cost (~$442 million).

In FY2024 the company acquired its Mexican partner operations for ~ $ 150 million. This was buying back franchise rights in a profitable market, which allowed lululemon to capture the full retail margin and control the brand experience. Unlike MIRROR, this is a low-risk deployment of cash with immediate accretion to OCF.

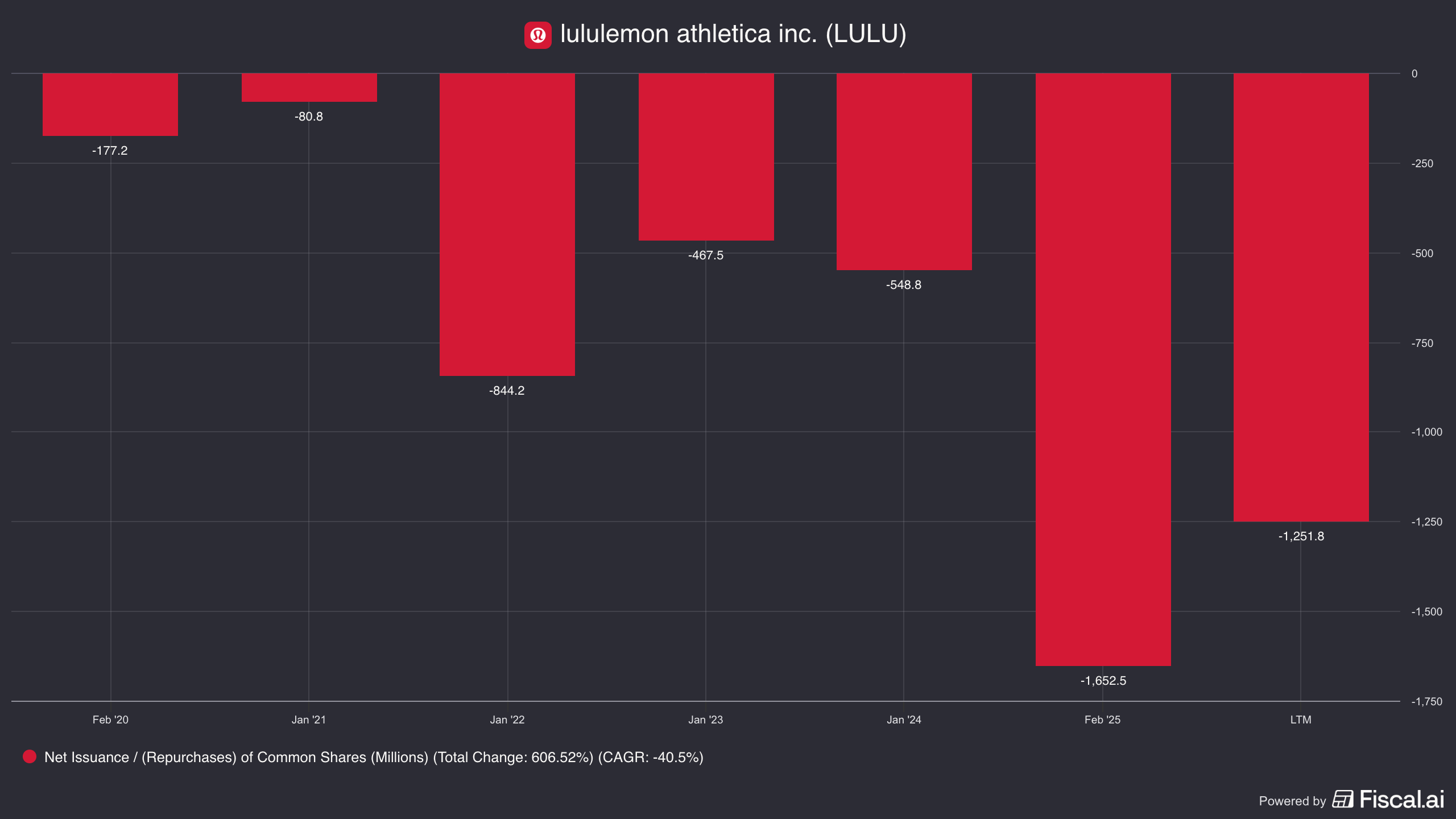

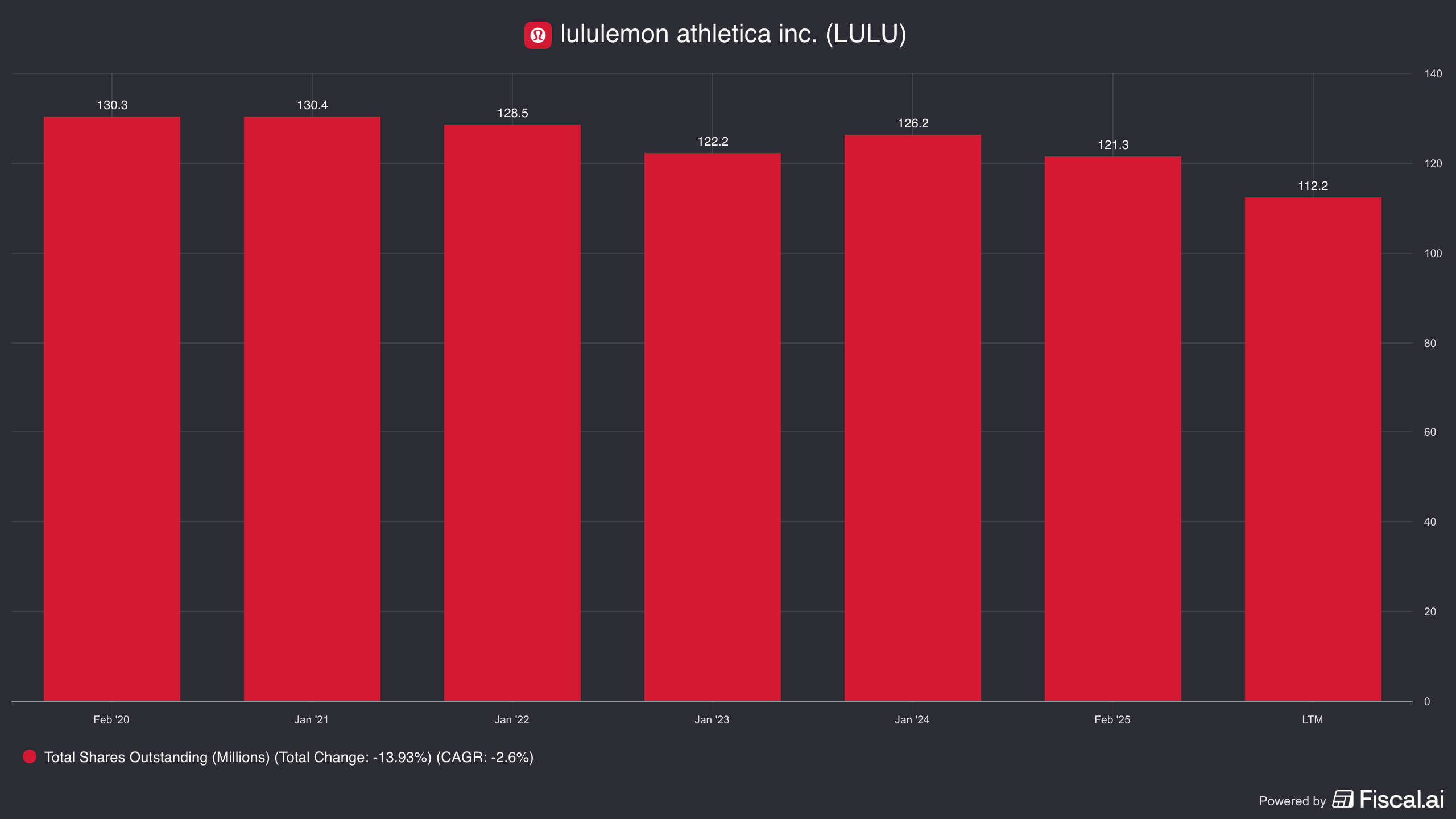

Share Repurchases

While historically the company retained cash, it is now spending to reduce the share count, repurchasing 5.1 million shares in 2024 alone. As of the last twelve months lululemon has been directing ~2/3 of its operating cash flow towards share repurchases.

This has resulted in a share count that is shrinking by about a ~2% CAGR over the last five years, although that is accelerating.

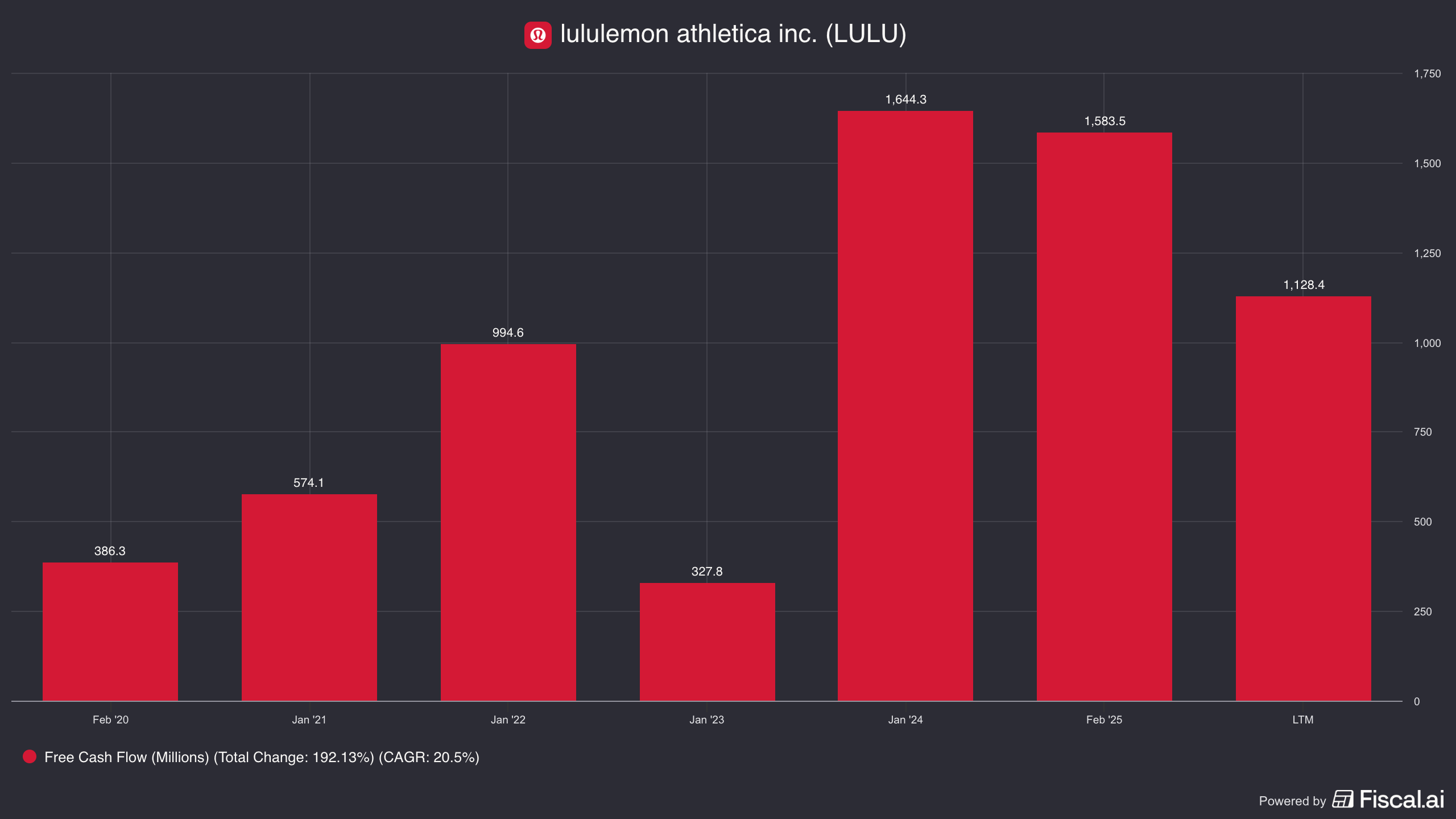

Free Cash Flow

The company’s ability to generate $1+ billion in FCF, while executing buybacks and while self-funding international revenue growth places it in the upper echelon of retail.

However, the current deterioration in OCF in FY2025 serves as a warning - the external environment is becoming more hostile, and this will inevitably be reflected in its near future FCF generation.

The Balance Sheet

At first glance, lululemon’s balance sheet looks impeccable, especially for a retailer. Currently it has about $1 billion of cash and cash equivalents on its balance sheet, with zero long term debt.

However, digging deeper there are two warning signs flashing.

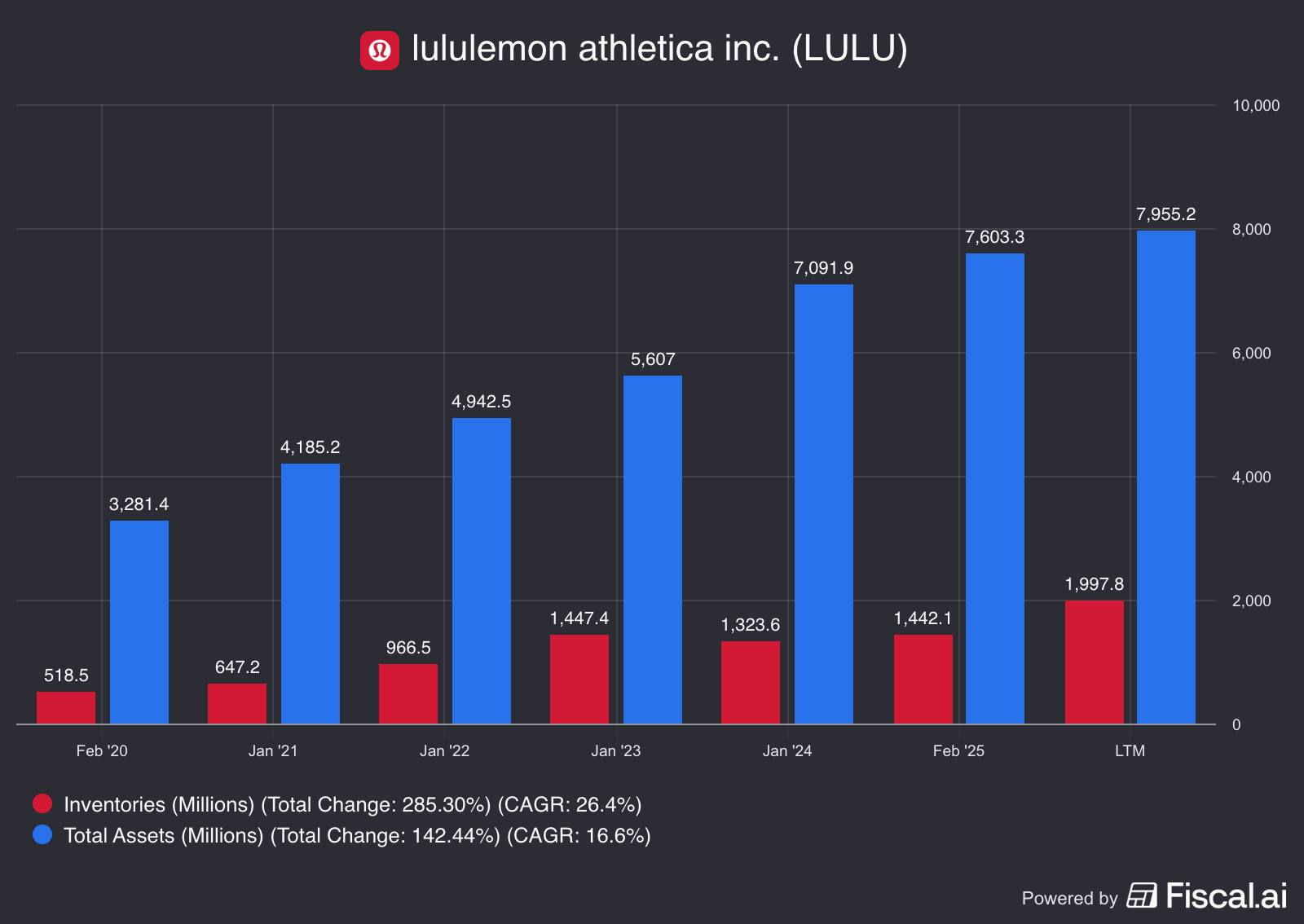

The Inventory

Inventory levels have generally been growing with time, which makes sense as inventory is the lifeblood of a retailer. However, as a proportion of total assets, it’s climbing back to about 25%.

The last time it approached these levels was in 2023, where lululemon had to take delivery of a large bolus of inventory, secondary to supply chain shocks. However, this time the inventory glut is secondary to a more concerning issue.

In the most recent quarter (Q3 2025) inventory levels increased 11% to $2.0 billion, outpacing sales growth of 7%. When inventory grows faster than sales, it suggests that the company misread demand and will likely need to continue markdowns in Q4 to clear the channel. The slower the inventory turn, the slower cash generation becomes.

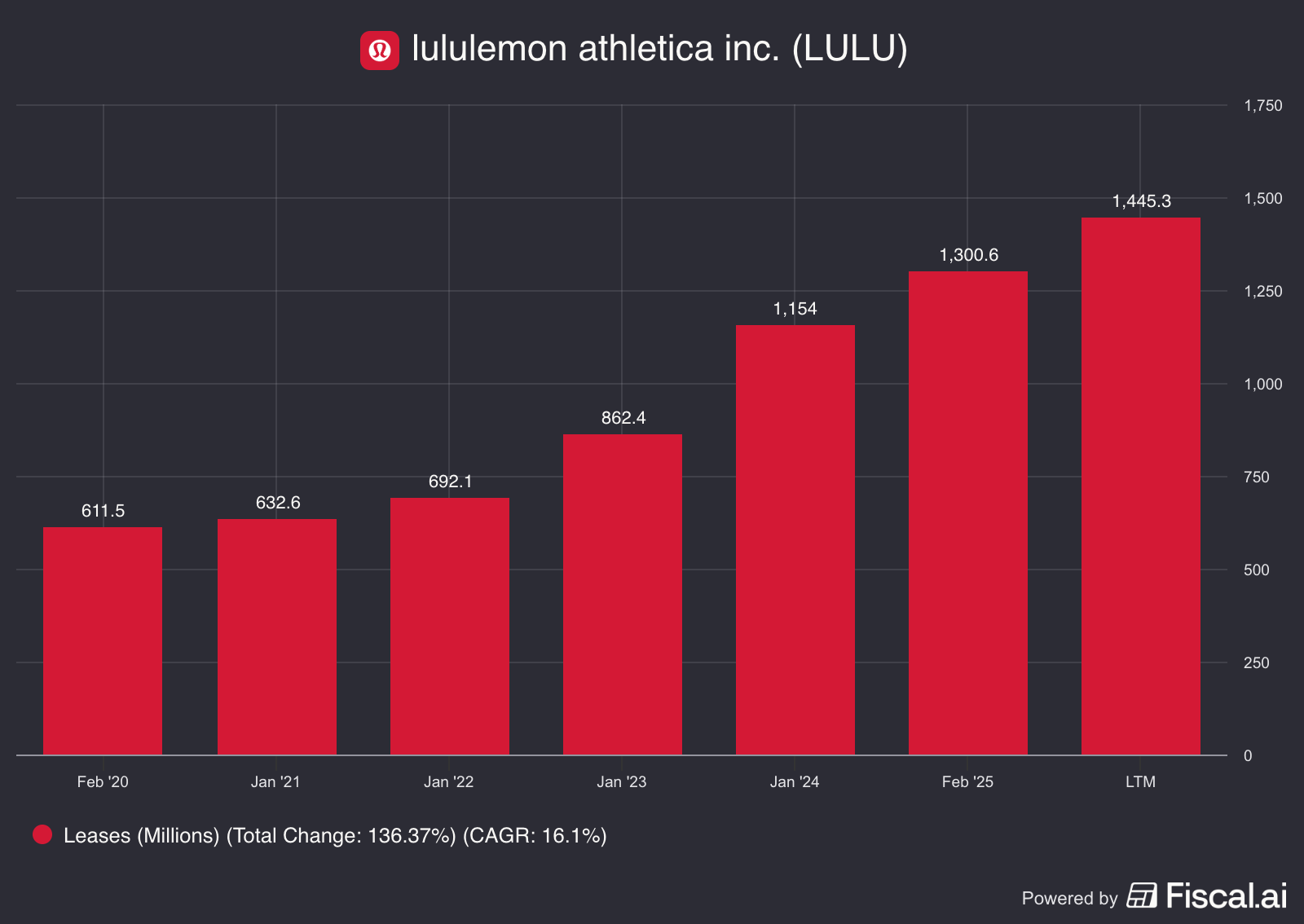

Lease Liabilities

The company’s growth model - opening new company-operated stores - requires signing 5-to-10 year commercial lease agreements. These agreements are effectively financing vehicles, as the landlord provides the capital (the store shell), and lululemon agrees to a stream of payments (rent) that amortizes this capital with an implicit interest rate (the incremental borrowing rate).

Unsurprisingly, as the company grows its lease liabilities have also grown.

It’s worth noting though that lease liabilities have more than doubled since 2021, growing at a 20% CAGR. This growth rate is outpacing the new store growth rate over the same time-period (~8% CAGR) indicating that lululemon is securing larger, more expensive "experiential" spaces in prime locations to compete with brands like Alo Yoga and Nike. The shift from smaller mall footprints to large-format flagship stores increases the fixed nature of the company’s cost structure.

“lululemon’s new SoHo flagship is located at 524 Broadway in New York City, spanning more than 17,000 square feet across two floors, and ranking among the brand’s largest stores worldwide.”

Now that we’ve covered the financial statements, let’s address the elephant in the yoga studio - Elliott Management.

The Activist: Elliott Management

In December 2025 Elliott Management built a ~ $1 billion stake in lululemon. Further, it is rumored that Elliott is pushing for Jane Nielsen to take over the leadership reins from recently departed CEO Calvin McDonald.

Jane Nielsen has substantial retail management experience, navigating the turnaround of both Ralph Lauren and Coach (now Tapestry). Her experience specifically