The Prancing Horse Accelerates

A Q3 2025 Update on Ferrari’s Four Pillars of Quality

Hey reader, welcome back 👋.

On Nov 4 Ferrari reported their Q3 2025 and below you’ll find an update on my thoughts. This article builds on our first Ferrari article from Oct 2025 and so please check that one out if you haven’t already

Source: Q325 Results Slide Deck

Our thesis for owning Ferrari N.V. (RACE) has always been straightforward: an ultra-luxury brand, not an automaker, compounding value through scarcity, pricing power, and peerless margins. The recent Capital Markets Day (CMD) on October 9, 2025, affirmed this strategy with conservative yet structurally strong 2030 targets. Now, with the release of the Q3 2025 we have empirical confirmation that the company is executing flawlessly against that blueprint, validating its standing as a world-class compounder.

Our view is that the Q3 performance is another step in dispelling the market skepticism following the CMD. Ferrari continues to demonstrate superior quality of execution, turning controlled volume into exceptional profitability. Here is an update on how the Maranello machine fared through the lens of the Four Pillars of Quality.

I. Pillar 1: Durable Competitive Advantage (The Moat in Motion)

Ferrari’s enduring advantage is rooted in its ability to generate high financial returns from limited production volumes. The Q3 2025 results underscore the success of the scarcity engine, even as the product portfolio shifts.

In Q3 2025, total shipments were largely flat year-over-year at 3,401 units. Crucially, despite this flat volume, net revenues grew by a robust 7.4% (9.3% at constant currency) to €1,766 million. This performance confirms that the primary lever for revenue and profit expansion is not volume, but mix and personalization.

Source: Q325 Results Slide Deck

The mix/price variance was a positive €25 million, driven overwhelmingly by the enriched product selection, particularly the ramp-up in deliveries of the ultra-high-margin SF90 XX and the newly introduced 12Cilindri families. This premiumization momentum effectively offset pressure from higher U.S. import tariffs and the planned phase-out of the limited-series Daytona SP3.

The order book remains robust, extending well into 2027, providing exceptional revenue visibility, and further suggesting that the CMD 2025 guidance management provided is a bear case. Regardless, the structural demand allows management to remain disciplined in controlling output, protecting brand exclusivity, and commanding unrivalled pricing power in the luxury segment.

Electrification and Product Cadence Confirmed

Management continues to navigate the technological transition with a calculated pace, preserving the core DNA of the brand. CEO Benedetto Vigna affirmed that the company is defining a “clear trajectory... setting the floor for sustainable growth toward 2030” and is committed to demonstrating that the “Ferrari Elettrica—will once again drive innovation”.

The product pipeline is actively supporting the high-margin mix shift. Q3 deliveries were led by the Purosangue SUV, the 296 GTS, the 12Cilindri family, and the Roma Spider. Looking ahead, the recent unveiling of the Amalfi and 849 Testarossa families will further support the order intake, ensuring a continuous cadence of fresh, highly profitable models to replace existing ones like the SF90 and 296 GTB as they approach the end of their lifecycle.

II. Pillar 2: High and Stable Capital Returns and Profitability

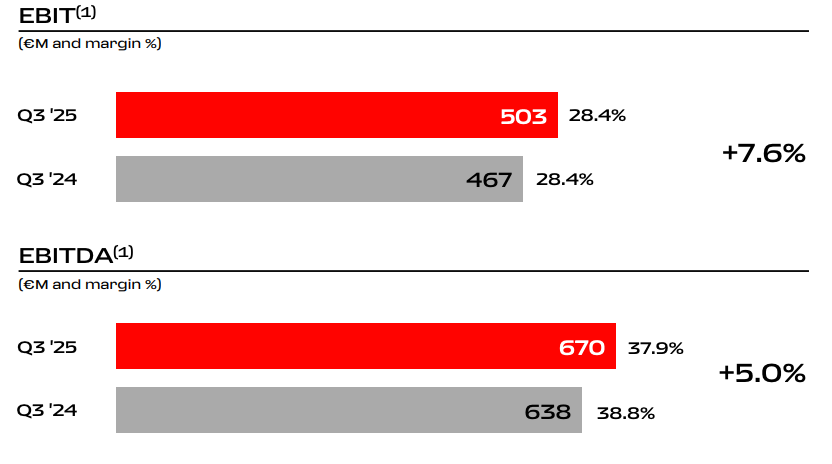

The Q3 2025 figures confirm Ferrari’s industry-leading profitability and its relentless march toward the minimum 40.0% EBITDA margin target by 2030.

Exceptional Margins: Q3 Adjusted EBITDA reached €670 million, translating to a powerful 37.9% margin. This remains one of the highest profitability metrics in the entire global luxury and automotive landscape, validating the economic returns discussed in our initial analysis. Operating Profit (EBIT) grew 7.6% year-over-year to €503 million, achieving a 28.4% margin.

Quality of Revenue Translates to Profit: The fact that both EBIT and EBITDA grew healthily despite flat volume growth is definitive proof that the quality of revenues—derived from a richer mix and soaring personalization revenues—is successfully expanding gross and operating margins.

Source: Q325 Results Slide Deck

Tax Efficiency: The effective tax rate in Q3 was a favourable 22.0%, benefiting from the new Patent Box and tax incentives for eligible R&D costs , thereby maximizing the conversion of operating profit into net profit.

This accelerating profitability trajectory places the company well on track to exceed its 2026 profitability targets one year ahead of schedule, a key forecast confirmed during the CMD.

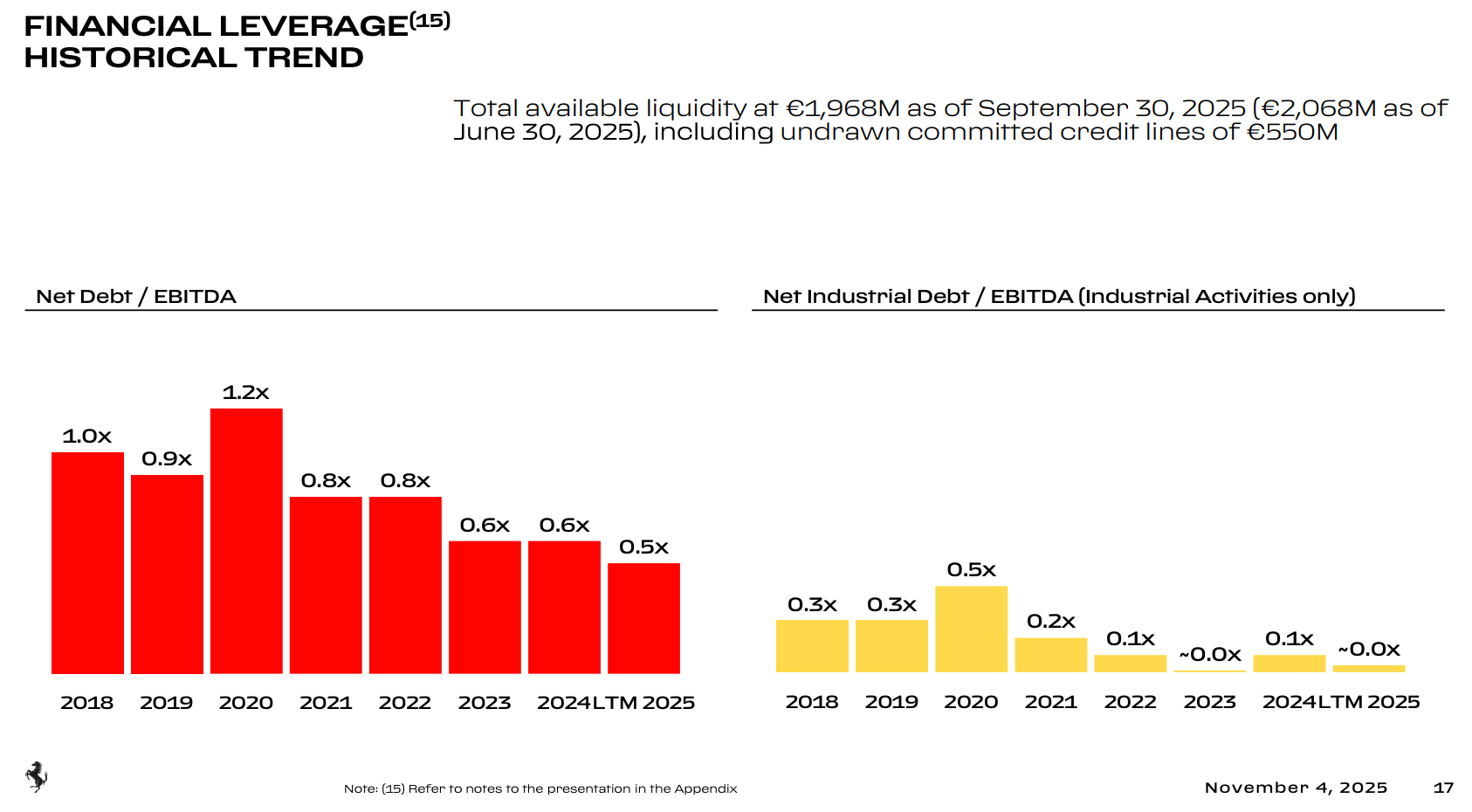

III. Pillar 3: Financial Strength and Balance Sheet Safety

The balance sheet reflects a core industrial business that operates with minimal leverage, providing substantial capital flexibility and safety, which is paramount in a quality investment framework.

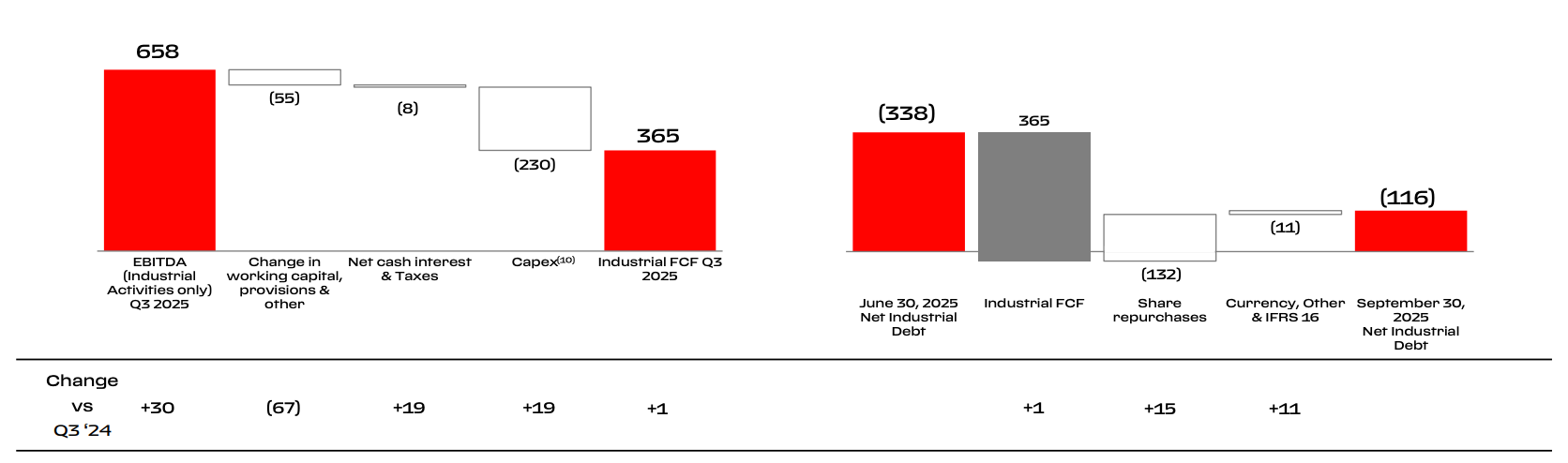

Pristine Industrial Liquidity: The company maintained its exceptional financial discipline, reducing Net Industrial Debt to a minimal €116 million as of September 30, 2025, down significantly from €338 million in the prior quarter. This near-net-cash position for the core manufacturing business effectively eliminates industrial solvency risk, providing management with maximum flexibility to execute its ambitious CapEx plan (€4.7 billion for 2026-2030).

Source: Q325 Results Slide Deck

Strong Cash Generation: Industrial Free Cash Flow (I-FCF) generation was r €365 million in Q3, and relatively flat year over year. Ferrari continues to reinvest in their business, with €230 million of capex in the quarter. They continue to reward shareholders with ongoing buybacks, spending €132 million on repurchases.

Source: Q325 Results Slide Deck

IV. Pillar 4: Visionary Management and Capital Allocation

Management’s quality is defined by its ability to stick to a clear strategy and allocate capital effectively between long-term growth and immediate shareholder returns.

Capital Deployment: Management continues to balance strategic investment (CapEx of €230 million in Q3 toward product and infrastructure development) with direct shareholder returns (share repurchases of €132 million in the quarter, completing the multi-year €2 billion program one year ahead of schedule).

Innovation Driving Mix: The success of the newly introduced SF90 XX and 12Cilindri families in driving the Q3 mix confirms that R&D investment is being successfully translated into higher-margin products. Furthermore, the continued development and unveiling of new high-performance models like the Amalfi and 849 Testarossa demonstrates a clear product roadmap that will sustain premium pricing into the future.

The Verdict

The Q3 2025 results are an unqualified success, confirming that the foundation of the Ferrari compounding thesis—pricing power and margin expansion driven by exclusivity—is stronger than ever. The operating results provide a strong and necessary counter-narrative to the market’s initial lukewarm reaction to the CMD guidance. The business continues to exceed management’s stated expectations, and they’ve shown a consistent history of under promise and over deliver. While macro risks persist (FX and tariff headwinds were noted as partial offsets in Q3 ), the exceptional financial cushion and pricing power remain the primary defence.

The core challenge remains reconciling the demanding current market valuation with management’s deliberately conservative guidance. However, continuous outperformance, confirmed by this quarter’s stellar results, suggests management is setting a low floor from which to consistently beat and raise expectations, securing the path for long-term compounding. We are buckled in and look forward to seeing where Ferrari takes us in the long term ride.

Thanks for reading, and join us next time.

Happy Compounding,

The Pursuit of Compounding 📈

PS: Like what you read? Buy us a coffee!

Disclaimer: We are private investors and not financial advisors. This post is for educational purposes only and does not constitute financial advice. Ferrari (RACE) is a stock we currently own. Always conduct your own due diligence before making any investment decisions.