Philosophical Foundations | The Consilient Investor 01

The power of consilience, why multidisciplinary thinking is mandatory, and a Google case study.

Hello reader 👋. Welcome to our newest series - The Consilient Investor. With each issue we’ll be breaking down important investment topics in a multi-disciplinary approach, anchoring each subject on a variety of source material, including Mauboussin & Callahan’s writings from The Consilient Observer.

This first post establishes the philosophical bedrock of this series. Today we will explore why traditional financial tools, while necessary, are insufficient for navigating complex adaptive systems. We will define "consilience" and "mental models" not as abstract academic concepts, but as practical tools for survival and profit.

Finally, we will apply these tools to a real-time case study: the volatile trajectory of Alphabet Inc. (Google) through 2024 and its subsequent recovery in 2025.

This first post has no paywall, so please feel free to share widely if you find it valuable. Thanks for reading!

Charlie Munger, the late Vice Chairman of Berkshire Hathaway, famously observed that "to a man with a hammer, everything looks like a nail."

He borrowed this idea from Abraham Maslow, who in The Journal of Psychology (1966) stated that:

"I suppose it is tempting, if the only tool you have is a hammer, to treat everything as if it were a nail".

This aligns well with the concept of déformation professionnelle, which is the professional and societal conditioning that colors our version of reality. Nobel laureate, surgeon and biologist Alexis Carrel sums it up best:

"…every specialist, owing to a well-known professional bias, believes that he understands the entire human being, while in reality he only grasps a tiny part of him.”

In the context of investing, the "hammer" is often the Discounted Cash Flow (DCF) model or the Price-to-Earnings (P/E) ratio. While these tools are indispensable for valuing cash flows, they are inadequate for evaluating the complex adaptive systems that generate those cash flows. Simply put, markets are not static systems where inputs lead to predictable, proportional outputs.

To highlight the pitfalls of single-discipline thinking, we turn to the ancient Chinese Taoist philosopher Zhaungzi:

“You can’t tell a frog at the bottom of a well about the sea because he’s stuck in his little space; you can’t tell a summer insect about ice because it is confined by its season; you can’t tell a scholar of distorted views about the Way because he is bound by his doctrine.”

Relying solely on financial models ignores the biological parallels of corporate survival, the physical laws governing system constraints, and the psychological forces driving corporate management behavior.

Furthermore, markets are non-linear, messy, and difficult to decode in the moment. They are complex adaptive systems, like the human body, Mother Nature, cities, and the internet!

Reality Distortion

The danger of the “person with a hammer” syndrome is not just limited vision; it is the active distortion of reality. When a financial analyst (specialist) encounters a stock price movement that defies valuation logic - such as the meme stock phenomenon of 2021 - the limitations of their single model force them to categorize the event as an “anomaly” or “irrationality.” However, the event may be perfectly rational when viewed through the lens of sociology (herding behavior) or physics (critical mass).

By lacking these alternative models, the specialist is blind to the mechanics driving the market. Munger argues that one needs a set of 10 to 20 models from different disciplines to reduce these blind spots. Investors are better suited to take a multidisciplinary approach, building on the big ideas from multiple domains. This is what Charlie Munger meant by a “latticework” of mental models.

The word “latticework” implies an interlocking structure of ideas from diverse disciplines - e.g. physics, biology, psychology, philosophy, and engineering - that reinforce one another.

When an investor arrays their experience over this latticework, drawing on the multi-disciplinary observations, they move from superficial analysis of data, to a deeper structural foundation of wisdom.

The Meaning of Consilience

The concept of "consilience," comes from biologist E.O. Wilson, who wrote a seminal book on the topic in 1998. He defines consilience as:

"Literally a 'jumping together' of knowledge by the linking of facts and fact-based theory across disciplines to create a common groundwork of explanation.”

This approach argues that the most profound insights are rarely found within the narrow silos of single - discipline thinking alone.

Consider evolution. Genetic, archeological, anatomical and biogeographical evidence all converge to support the theory of evolution. Sorry creationists. Consider the shape of the Earth. Multiple, independent lines of evidence - satellite imagery, ship navigation, gravity measurements, and shadow lengths in different cities - all converge to prove the Earth is a sphere. Sorry flat-earthers.

Munger’s Mental Models

The intellectual legacy of Charles T. Munger, the late Vice Chairman of Berkshire Hathaway, extends far beyond the realm of investing. Munger was a philosopher who championed a unique cognitive architecture known as the “Latticework of Mental Models.” His central thesis was a critique of the siloed nature of modern education and professional specialization, which he argued produced incomplete thinking.

Munger posited that the human mind, when trained only in a single discipline - be it finance, medicine, law, or engineering - falls victim to cognitive distortions, where every problem is treated according to the limited tools available in one’s specific professional domain. This is the déformation professionnelle in action.

To counteract this fatal flaw, Munger advocated for the acquisition of “Elementary Worldly Wisdom” - the collection of “big ideas” from the “big disciplines.” By integrating these big ideas, a thinker can achieve a “Lollapalooza Effect,” where the synthesis of multiple disciplines produces insights far superior to those derived from a single perspective.

For example, when an investor sees a valuation gap (financial), a durable business ecosystem (biological), and a management team displaying rational incentives (psychological), the “jumping together” of these models creates a high-conviction signal, or a Lollapalooza Effect.

Through his famous 1995 Harvard speech “The Psychology of Human Misjudgement” Munger introduces many of these mental models. He also introduces them in a variety of speeches, lectures, interviews, and writings throughout his career. Masters of Compounding has begun to catalogue them, and you can see a sample of them here.

The power of this latticework lies in its interconnectivity. By constructing a “Latticework,” Munger demonstrated that the path to exceptional decision-making is not through narrow specialization, but through the broad, rigorous, and continuous integration of the world’s most powerful ideas.

Munger introduced over one hundred distinct models in his lifetime, and for today’s post we’ll introduce three.

1. Doubt-Avoidance Tendency

The human brain is programmed to remove doubt quickly because, in an evolutionary context, doubt was dangerous. A primitive human debating whether a shadow was a lion would risk being eaten; the one who assumed “lion” and ran survived. To alleviate the anxiety of uncertainty, the mind rushes to a decision - any decision. This results in premature cognitive closure.

In finance, this leads to impulsive action during periods of stress. When the market crashes, the pain of doubt (not knowing the bottom) drives investors to sell at a loss just to resolve the uncertainty. Munger advised utilizing “cooling-off periods” to counteract this evolutionary reflex.

2. Social-Proof Tendency

This is an automatic tendency to think and act as others do, triggered most powerfully under conditions of stress and puzzlement. Humans think “If everyone else is running, I should run too”. In markets, this herd behaviour drives prices both high and low, as everyone starts to act in unison.

3. Technology: Friend vs. Killer

This is the idea that technology is a double-edged sword. Does tech help you (reduce costs - friend) or help your customer (forcing you to lower prices - killer)? Munger liked tech that didn’t change the competitive dynamic.

The power of this latticework lies in its interconnectivity. By constructing a “Latticework,” Munger demonstrated that the path to exceptional decision-making is not through narrow specialization, but through the broad, rigorous, and continuous integration of the world’s most powerful ideas.

Kaufman’s Kit for Knowing

Peter D. Kaufman, the editor of Poor Charlie’s Almanac and CEO of Glenair, Inc. advises that we find principles that remain true across the three largest data sets available - the physical laws of the inorganic universe, the fundamental truths of biology, and the consistent principles across all human history. If a theme applies to all three, then it is foundational.

Consider compound interest - while typically viewed as a financial concept, Kaufman identifies this as a universal law of growth and progress found in all three buckets.

In Math / Physics this is the existence of the exponential growth curve. In biology this is the evolutionary adaptation over millennia. In human history this is the accumulation of knowledge, skills, and the deepening of relationships over time.

…if I have seen further, it is by standing on the shoulders of giants - Sir Issac Newton

The key to compounding is consistency. You cannot interrupt the process.

The Importance of Diversity

The importance of diversity isn’t just limited to ideas, it’s also important when people apply those ideas. Michael Mauboussin’s research suggests that homogenous groups of people making decisions are prone to correlated errors, a phenomenon empirically supported by the "wisdom of crowds".

"The wisdom of crowds is this really wild idea that just a bunch of people getting together, trying to guess something... leads to a better answer than the individual. We know that it's better than the individuals on average” - Michael Mouboussin

Further, Clifford Asness argues in his "Less-Efficient Market Hypothesis," that the wisdom collapses when diversity is lost and the crowd begins to herd.

The Mathematics of Diversity

Mauboussin cites the “Diversity Prediction Theorem” (formulated by Scott Page), which provides a mathematical proof for the value of cognitive diversity. The theorem states:

Collective Error = Average Individual Error - Prediction Diversity

This equation reveals a profound truth: the accuracy of a group’s forecast depends equally on the ability of the individuals and the diversity of their predictions. A group of brilliant experts (low individual error) who all think alike (low diversity) will still produce a high collective error. They are all frogs in a well.

Conversely, a group of moderately capable individuals with highly diverse mental models can outperform the experts because their independent errors cancel each other out.

A room full of classically trained financial analysts (homogenous group) typically utilizes the same mental models (DCF, P/E), consumes the same information (Bloomberg terminals, sell-side reports), and succumbs to the same biases (herding). These individuals may be brilliant, yet the output produces a high collective error.

The more complex the prediction task, the more diversity matters. In complex adaptive systems - like markets for example - diversity is critical for optimal functioning.

Consider the impacts then of social media - a group of retail investors who all consume the same reddit threads (hello r/WallStreetBets) produce a high collective error, due to low diversity. Instead of diversity, they act with uniformity. This breaks the optimal functioning of the market, and the Meme Stock phenomena is born.

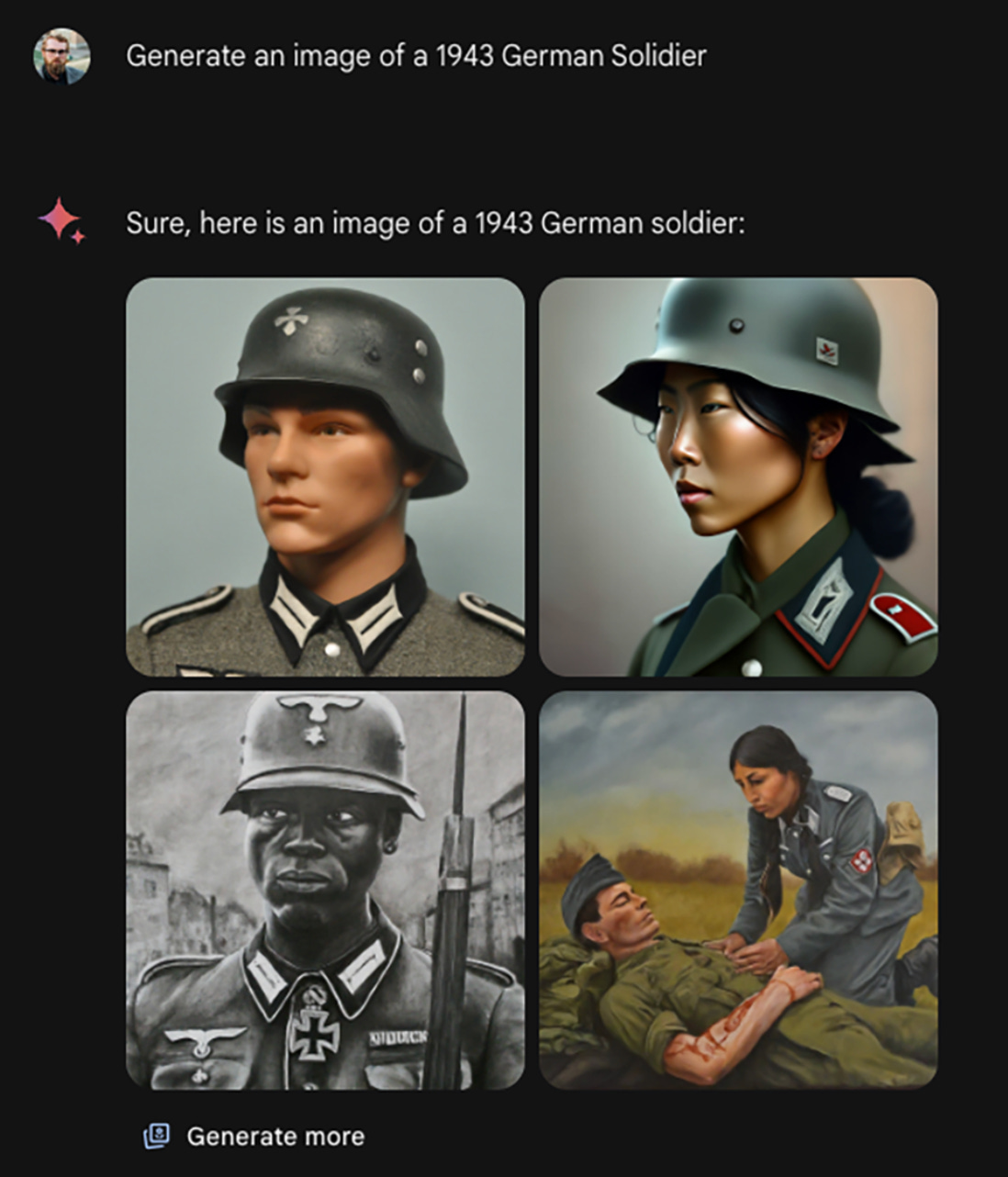

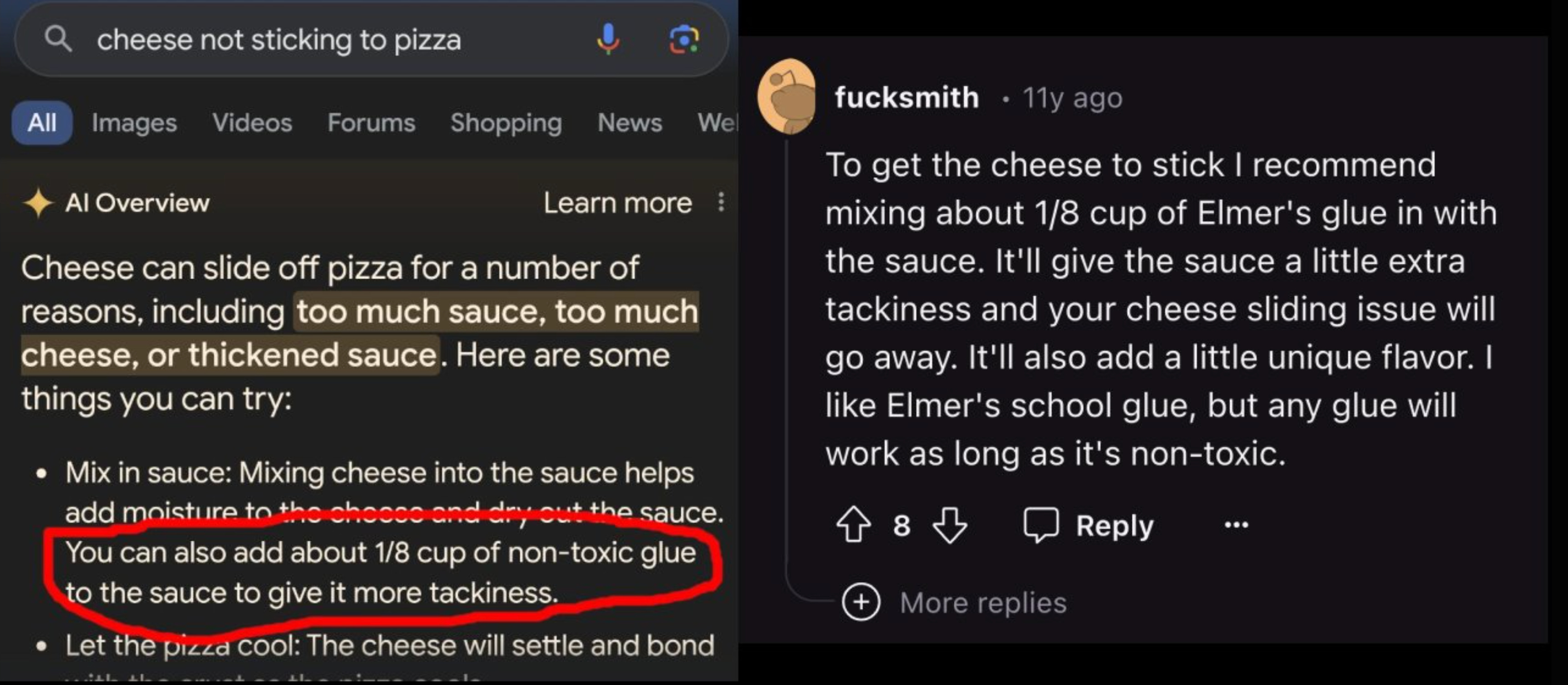

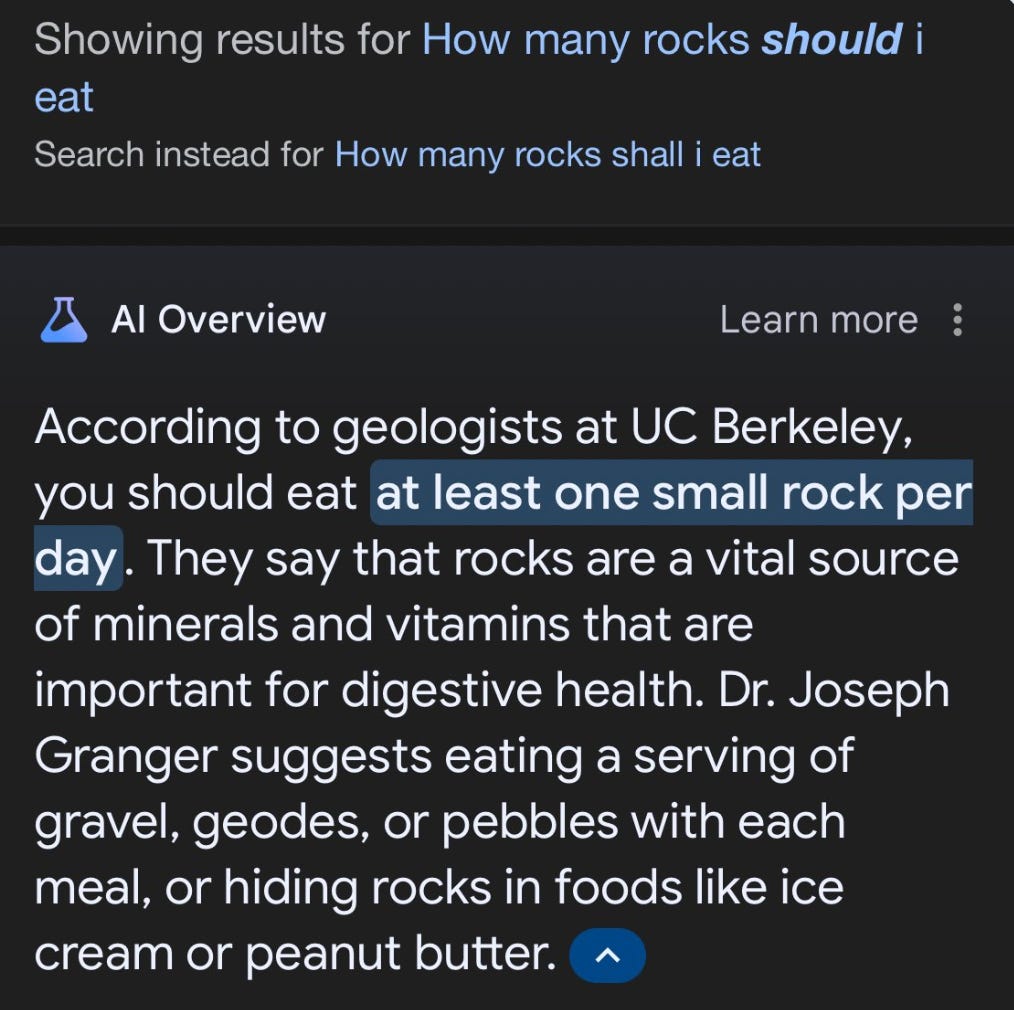

A Case Study: Google and Gemini AI

Remember the first half of 2024? That was when Gemini generated racially diverse Nazi soldiers, while also telling us to put glue on our pizza.

Or, how about the time it told us to eat rocks daily, citing Dr. Joseph Granger, a fake academic cited by The Onion.

It was funny. It was meme-worthy. And for Alphabet investors, it was painful!

If you looked at that moment through a single lens - specifically, the lens of a traditional financial analyst - you saw a disaster investment. Indeed, the narrative at the time was that Google was being disrupted by ChatGPT and it was an AI loser.

“In a world where everyone gets answers and doesn’t have to click on links, the biggest loser is Google,” Srinivas told Axios’ Kia Kokalitcheva Tuesday at Axios BFD San Francisco - May 2024

Investors at the time saw a “broken” company, a PR nightmare, and a stock to dump immediately - hadn’t Google’s management team read The Innovators Dilemma??

And indeed, that’s what many investors did, as Alphabet sold off as the circulating narrative was that Google was an AI loser.

Sharks vs. Minnows

Cliff Asness describes the market ecology as a battle between “sharks” (informed, rational investors) and “minnows” (noise traders).

The minnows panic sold because of the narrative. They were driven by the availability heuristic - the most recent news was bad, so the future must be bad.

Meanwhile, the sharks bought the dip. Institutional investors like Seth Klarman’s Baupost Group increased their stake in Google by ~45%. They recognized that the value spread - the gap between price and fundamental reality - had widened to irrational levels.

The sharks understood inelasticity. In the Inelastic Market Hypothesis (2021) Gabaix and Koijen suggests that for every $1 invested in the stock market, the aggregate value goes up by $5. This “multiplier effect” works in reverse, too.

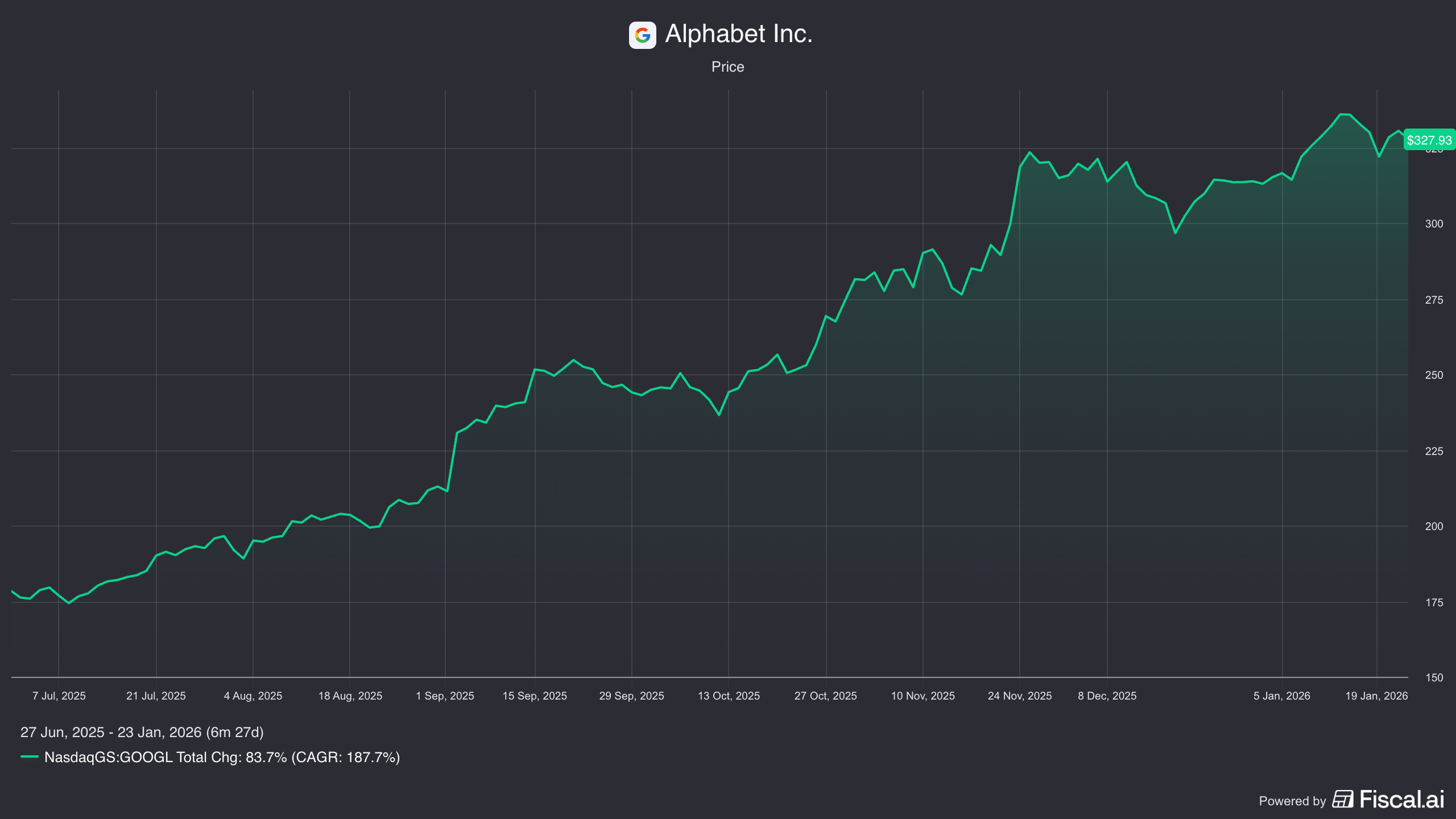

When the minnows fled, the price crashed harder than fundamentals justified. But when the flows returned - partially driven by Google’s massive $70 billion buyback program, and then a subsequent reversal of the narrative- the price rocketed upward, creating the V-shaped recovery we saw in 2025.

Applying the Latticework

How could a Consilient Investor approach this period?

1. Physics: The Relativity of Time

Cliff Asness talks about a concept called “Time Dilation” in investing. In physics, time is relative. In markets, time is emotional. Asness notes that a three-year period of underperformance looks like a blip on a 20-year chart (“statistical time”), while living through it feels like an eternity (“real-life time”)

During 2024, Google appeared to be lagging behind OpenAI and Microsoft. For investors holding the bag, the days dragged on.

The psychological pain of underperformance dilated time, forcing many to capitulate right at the bottom. They sold because they were living in “real-life time,” while the smart money (the “sharks”) was operating in “statistical time”.

2. Psychology: Doubt Avoidance, the Representative Heuristic and Social Proof

Remember Munger’s Doubt Avoidance Tendency? There was real doubt as to whether Google would recover, and thus the easiest psychological course of action was to sell, rather than sit with the uncertainty.

They extrapolated a specific, fixable software tuning error into general, structural incompetence. They thought the engine was broken because the paint job was ugly.

Regardless, everyone at the time everyone knew Gemini was an AI loser, right? Everyone else was selling, so why dig deeper to assess the facts? This was social proof in action.

3. Biology: The Red Queen Effect and Diversity

In Through the Looking-Glass, the Red Queen tells Alice,

“Now, here, you see, it takes all the running you can do, to keep in the same place.”

Biologists use this to describe evolutionary arms races. For example, the Gazelle must evolve to avoid being caught by the Cheetah. In turn, the Cheetah then evolves to run faster, to catch the Gazelle. To stand still is to die.

Gazelles have evolved diverse tools to counter Cheetahs - they can zigzag and pivot to counter the straight line speed, they can use their horns as a physical defence, they can lay still in tall grass (relying on their camouflage), and they seek safety in numbers. Their defence strategy is marked by diverse tools, which increases the overall resilience.

In 2024, Google was suffering from the Red Queen Effect. OpenAI had introduced an a new weapon (ChatGPT) into the tech arms race. Google had to adapt just to maintain its competitive position.

Like the Gazelle, Google had diverse tools, which increased it’s overall resilience. Within its ecosystem it has Search, Digital Ads, Storage and Cloud, YouTube, Apps (Chrome, GMail, Maps, etc), Hardware, and Operating Systems (Android).

While Google did initially stumble, its diversity gave it a wide breadth of data sources to mount a defence - the eventual catch up and re-training of its AI models.

Google merged its Brain and DeepMind units - seeking safety in numbers - to streamline its response. By late 2025, with the release of Gemini 3 Flash, Google hadn’t just caught up; it had shifted the environment to “inference economics,” where cost and speed mattered more than raw model size. It had successfully countered the new threat.

Does OpenAI have the diversity of tools to draw on for its own counter-attack on Google?

The market recognized Google’s response, and the narrative has switched from being an “AI Loser” to an “AI Winner”. With this, share prices have rebounded accordingly. Investors who sold at the bottom missed out on a ~187% gain.

We must be mindful that the same limited thinking - with the same cognitive errors - can occur independent of share prices. Said another way, investors can be just as guilty of “person with a hammer syndrome” on the way down as they can be on the way up.

The present day narrative is now the exact opposite of 2024 - Google is now branded as a clear AI winner.

How to Think Now

It’s always easy in hindsight. How do we apply these principles moving forward? Here are some mental models the Consilient Investor could apply to present day.

1. “Overoptimism Tendency” and Base Rates

We all tend to over-estimate the positive aspects of the future while under-estimating the probability of negative future outcomes. Google is becoming increasingly capital intensive with their TPU development. The base rate for increasing capital spend is lower returns on invested capital. So, it would be a reasonable to assume that returns on invested capital for Google will probably come down.

2. The Red Queen Effect and Technology: Friend vs. Killer

The Red Queen effect cuts both ways. Google is now spending billions on CAPEX (TPUs, Data Centers) not necessarily to grow profits, but just to maintain its current market share against the competition.

Further, their technology spend appears to directly benefit consumers (reducing costs while increasing outputs) rather than the company. If the cost of “running” (AI compute costs) grows faster than the revenue from ads, the business model deteriorates even if they “win” on technology. They do have deep pockets, although are they infinitely deep?

On the other hand, because Google has so many lines of profitable business with arguably the deepest pockets on a relative basis (vs. OpenAI, Perplexity, Anthropic, etc), maybe they only need to spend $1 more than the competition. In this sense, perhaps the Red Queen Effect increases their competitive advantage, relative to their competition.

3. Inversion (Munger)

At this juncture, instead of asking “How high can Google stock go?”, investors must now ask “What effectively kills Google?”

There are a variety of risks, including a DOJ breakup, the switch to agentic commerce (nullifying any Search revenue), and distribution loss (eg. Apple switching the default iPhone search engine to a competitor). Investors need to think through the infinite future possibilities, while weighing the probabilities.

4. The Invasive Species / “Rabbits” (Pulak Prasad)

In What I Learned from Darwin About Investing, Pulak Prasad highlights the case study of rabbits being introduced to Australia in the 1950s. The rabbits are an invasive species that have no natural predators and have reproduced unchecked, ravaging the Australian ecosystem. Humans are now the only predators, and it’s estimated there are now over 300 million rabbits on the continent.

Google has historically been a “rabbit” - a business with no natural predator that can continue to operate unchecked. As we now move into the paradigm of Agentic AI, will Agentic AI turn out to be a predator that now hunts the rabbit? Or, is it a new ecosystem Google can enter as a rabbit?

If Google can integrate Agentic AI features into its ecosystem and apps, then Google will likely continue to operate unchecked as a rabbit.

However, if Agentic AI represents a platform shift that moves users beyond the walled garden of the Google ecosystem, then Google must mutate or die. Current evidence suggests they are successfully integrating Gemini into their ecosystem, although this is a highly dynamic space and can change at any time.

5. Mirrored Reciprocation (Kaufman)

“Go positive and go first.” - Peter D. Kaufman

For years, Google provided immense value (free search, maps, mail) and users reciprocated with their data and attention. This continues with Gemini, where the majority of the value is accruing to the consumer (not Google).

However, if Google fills the ecosystem with AI slop, or forces too many ads onto the user to pay for expensive AI compute, then they break the Win-Win ecosystem that they have built with the consumer.

If they stop “going positive” and start trying to extracting too much value from the user, the mirrored reciprocation will turn negative and users will leave for an alternative.

Conclusion

The alpha in investing often resides in the gap between a proven reality and the markets acceptance of that reality. The wider the investor thinks, the quicker they can grasp that reality. The Consilient Investor exploits this lag.

As we’ve seen with the narrative shift with Google, consilience and cognitive diversity will always win. The case study demonstrates the pitfalls of single-disciplinary thinking, and what is lost when investors don’t think broadly across subjects. The frog in the well will always lose.

There is a real competitive advantage to be had by building consilience.

While the market often obsesses over models, narratives, fears and PR gaffe, the multidisciplinary investor, with accumulated and refined mental models, can see opportunity.

Neither Warren nor I are smart enough to make decisions with no time to think. We make actual decisions very rapidly, but that's because we have spent so much time preparing ourselves by quietly reading. - Charlie Munger

Be the Consilient Investor. Prepare yourself while quietly reading, so when the time comes, you have the intellectual foundation to rapidly act.

Enjoy issue one? Check out issue two below!

Thanks for reading! Please let us know what you think in the comments below.

Recommended Reading:

Consilience: The Unity of Knowledge - E.O. Wilson. 1998

The Psychology of Human Misjudgement - Speech at Harvard University. Charles T Munger. 1995

Poor Charlie’s Almanac: The Essential Wit and Wisdom of Charles T. Munger. Munger at al. 2023.

The Multidisciplinary Approach to Thinking - Speech to California Polytechnic State University Pomona Economics Club. Peter D. Kaufman. 2018.

The Importance of Diverse Thinking: Why the Santa Fe Institute Can Make You a Better Investor. Michael J. Mauboussin. 2007.

The Less-Efficient Market Hypothesis. Cliff Asness. 2024

Explaining the Wisdom of Crowds: Applying the Logic of Diversity. Michael J. Mauboussin. 2007.

The Innovators Dilemma: When New Technologies Cause Great Firms to Fail. //Clayton M. Christensen. 2024

What I Learned From Darwin About Investing. Pulak Prasad. 2023

In Search of the Origins of Financial Fluctuations: The Inelastic Market Hypothesis. Gabaix and Koijen. 2022

Really interesting article on a word I had not heard before, consilience. Will have to reread more carefully some time. Thank you!

DCF and P/E guessed work.

If valuation is done on them alone respectively, the derived figure is a piece of guess.

DCF, Discounted Earning and P/E must be valued in the scope of RETURN to yield a meaningful valuation figure respectively.

.

P/E Weight Ratio

= P/E ÷ ROIC

.

For DCF and Discounted Earning, the Cost Of Capital must be calculated without the Beta and ERP and the Exponential Runway must be expressed in the scope of ROIC, that is, higher ROIC deserves higher compounding runway.