Medline (MDLN) Deep Dive: Quality Business, Complicated Structure

Unpacking the "Up-C" structure, the PE overhang, and why we’re waiting for a better price.

For decades, Medline Industries (MDLN) was the quiet giant of Northfield, Illinois. Founded by the Mills family (who started making butcher aprons in 1910), it grew into the backbone of the U.S. hospital system, delivering everything from surgical kits to bedpans.

In 2021, the family sold a majority stake to a “who’s who” of private equity—Blackstone, Carlyle, and Hellman & Friedman—in a massive $34 billion LBO. Fast forward to today: they’ve returned to the public markets in the largest IPO of 2025, selling ~248 million shares and raising over $7 billion to clean up their balance sheet.

Here is the question we seek to answer: Is MDLN a long-term compounder to buy and hold forever, or a private equity exit pump and dump?

Table of Contents

The Business:

Most investors try to box Medline in with the “Big Three” distributors: McKesson (MCK), Cardinal Health (CAH), and Cencora (COR), although this is a mischaracterization.

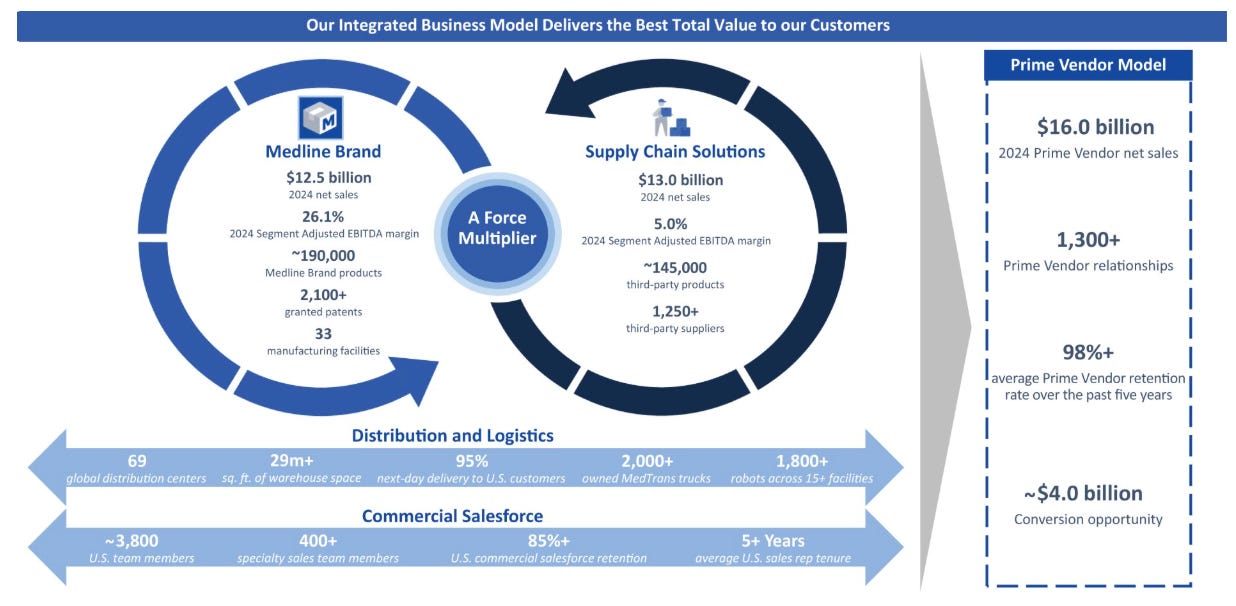

The “Big Three” are logistics companies. They move boxes from Point A to Point B for a razor-thin 1-2% margin. Medline is different. They operate a vertically integrated hybrid model that involves both manufacturing and logistics.

Manufacturing

It manufactures approximately 190,000 of the 335,000 products it sells. This portfolio includes essential, high-volume consumables such as surgical kits, gloves, protective apparel, incontinence products, and wound care supplies.

Logistics

Medline operates 69 global distribution centers comprising over 29 million square feet of warehouse space. It also owns and operates its own delivery fleet, “MedTrans,” consisting of over 2,000 trucks.

This network allows Medline to offer next-day delivery to 95% of the U.S. population. Following the COVID-19 pandemic, Medline invested heavily in inventory depth, positioning itself as the partner of choice for resilience. This capital-intensive strategy - holding more “safety stock” than competitors - has been instrumental in winning market share from rivals who operate leaner, “Just-in-Time” models that failed during the crisis.

Medline delivers both their own and third-party products. Their revenue is split about 50/50 between both.

The Prime Vendor Agreement

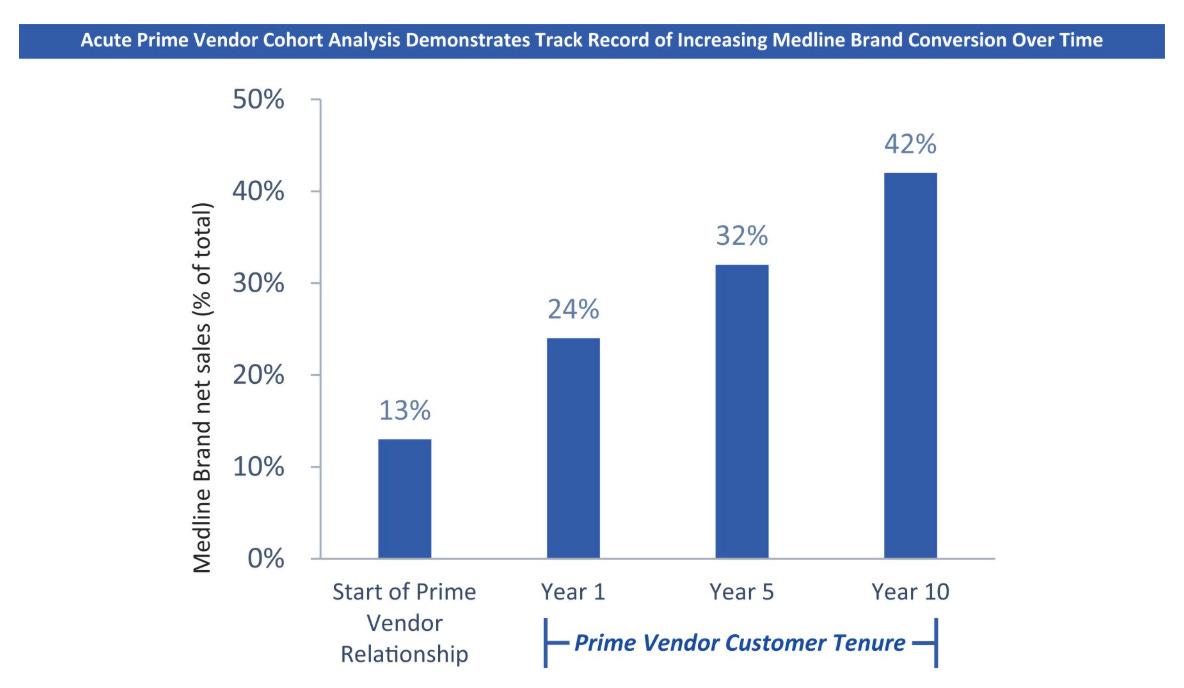

Once Medline is in a hospital, they execute a “land and expand” strategy. They identify high-cost items the hospital buys from 3M or J&J, and swap them out for a “Medline Brand” equivalent at a 15% discount. The hospital saves money, and Medline gets new business.

The engine of Medline’s growth is the Prime Vendor agreement. In these multi-year contracts (typically 5 years), a healthcare provider agrees to route the vast majority (>80%) of their med-surg spend (products, delivery) through Medline.

The retention rate for Prime Vendor customers stands at an impressive 98%, validating the stickiness of this service-heavy model. The hospital reduces its supply costs, while Medline - because it manufactures the product - earns a higher gross margin than it would have distributing the competitor’s product. It’s a win-win business model, that bodes well for positive sum value creation and long term compounding.

This sets them up for a scale economies shared model, where the more volume they control, the more they can manufacture for themselves, and thus the more they benefit from scale economies. This allows them to either expand their operating margins, or pass the savings onto their customers.

The Balance Sheet and the IPO: Cleaning Up the Mess

Medline initially filed to offer 179 million shares, but ultimately sold ~248 million shares at $29.00, raising gross proceeds of approximately $7 billion. This transaction stands as the largest U.S. IPO of 2025, surpassing all technology and industrial listings for the year.

The immediate secondary market reaction was euphoric. Shares opened at $35.00 and closed their first day of trading at $41.00, a 41.38% increase from the offering price. This pop added approximately $12 billion to the market capitalization in a single session.

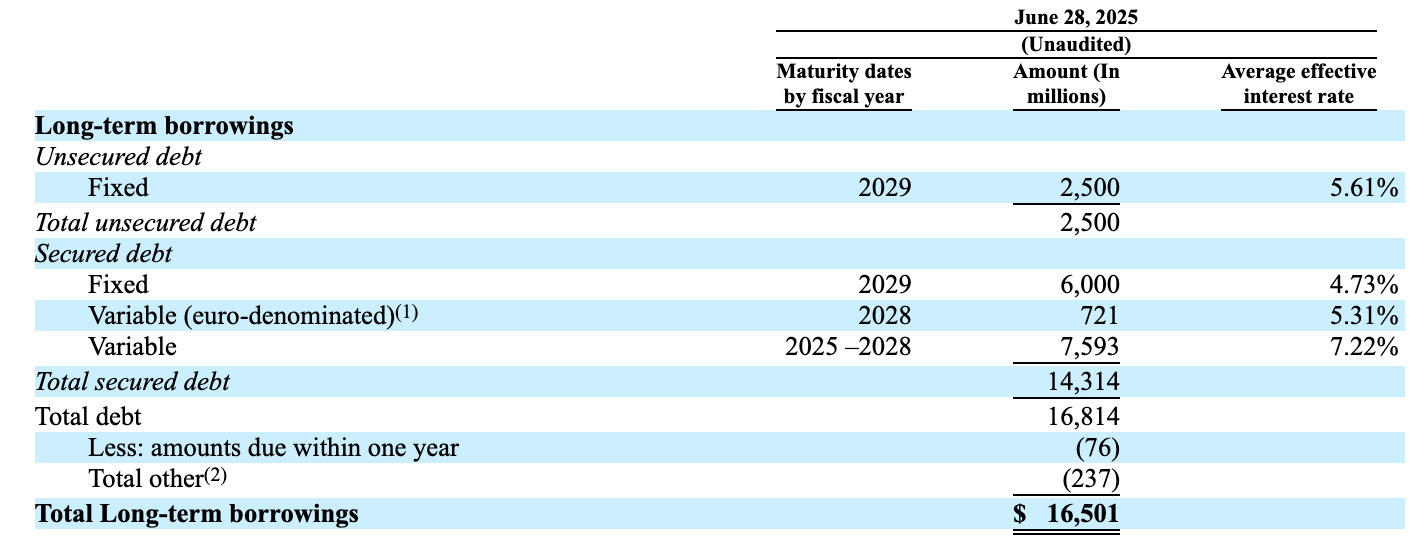

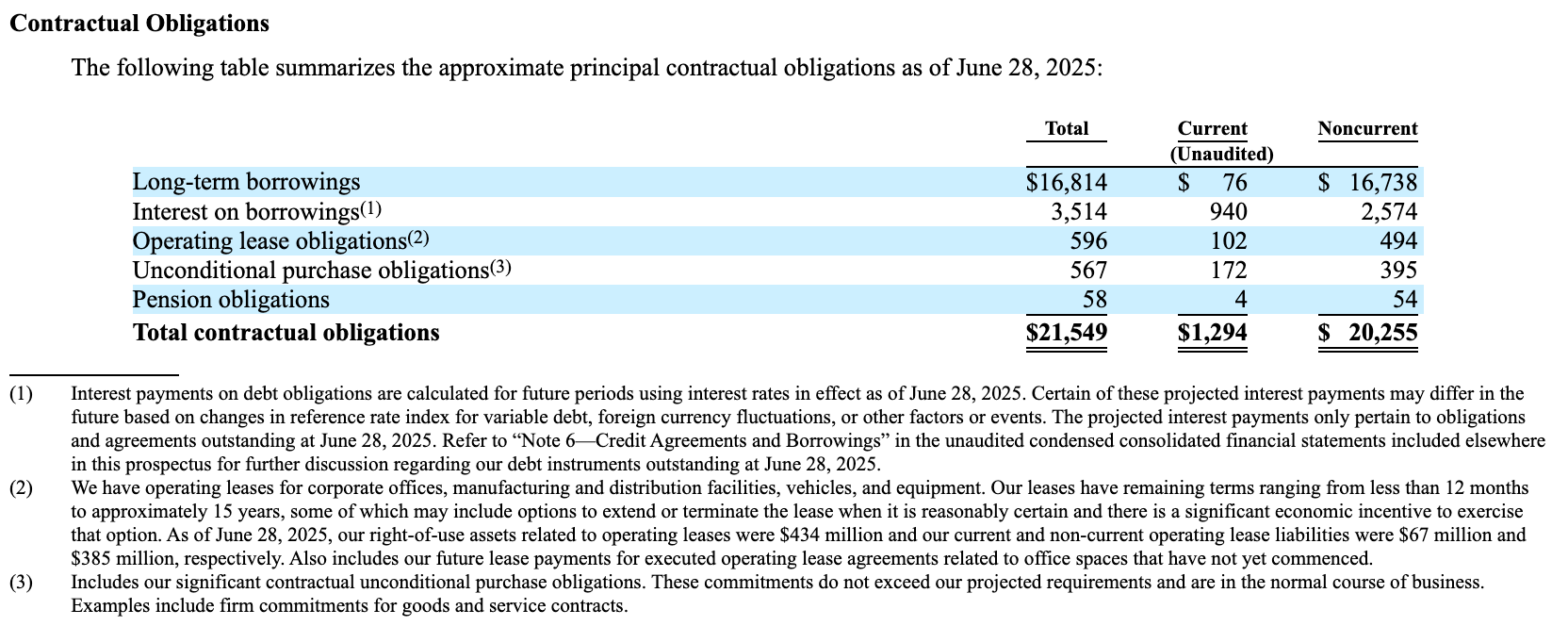

Debt

The primary goal of this IPO was balance sheet repair - specifically, fixing the debt load from the $34 billion Leveraged Buyout (LBO) in 2021. Pre-IPO Debt stood just shy of $17 billion, and it’s anticipated that ~$4 Billion of the IPO proceeds will go to debt repayment, dropping total debt to ~ $13 billion, saving ~$300 million in annual interest expense.

Looking deeper Medline does have some lease liabilities, pension liabilities, and purchase obligations that together add another $1.2 billion to their overall liabilities.

Private Equity Shares

On Medline’s balance sheet we see the various private equity shares listed as liabilities. They are stratified into tranches that define the order of operations for cash flow. This stratification is governed by the Limited Partnership Agreement (LPA), which serves as the constitutional document of the entity.

The S-1 filing indicates that Medline Holdings, LP operated under a strict “Distribution Waterfall,” a mechanism that dictates that cash distributions (other than mandatory tax distributions) must follow a rigid sequence of priorities before any general sharing of profits can occur.

The rationale behind this structure is the mitigation of principal risk for the primary capital providers—in this case, the private equity sponsors and the Mills family—while preserving significant upside leverage for the management team through incentive units. The Partners’ capital is divided into distinct share classes (Class A, Class B, and Class B CUPI) that then become “Common Units” in the post IPO structure. We’ll cover this more below.

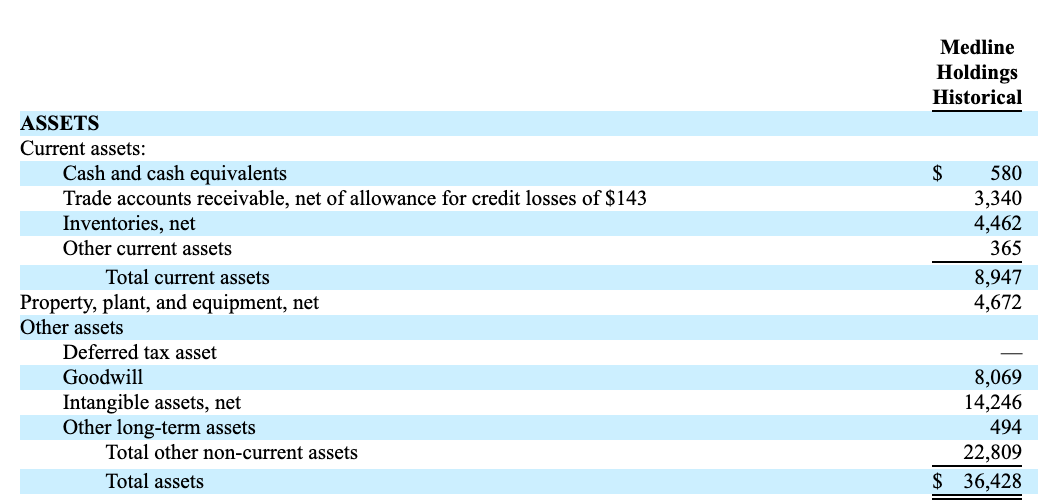

Assets

As of June 2025 the company held roughly $8 billion in Goodwill and $14.6 billion in Other Intangibles.

This is a byproduct of the private equity buyout accounting and represents the premium paid for the brand and customer relationships. As we’ll see below, this has material impact when we calculate Medline’s ROIC.

Medline also carried $4.46 billion in inventory as of June 2025. This is strategically high. Unlike competitors who optimize for “Just-in-Time” efficiency, Medline holds “Just-in-Case” buffer stock (safety stock), which helps them win contracts by guaranteeing supply during shortages.

We can see the remainder of their assets consists of Cash, Trade Accounts Receivables (reflecting credit terms extended to hospital systems), and Property, Plant & Equipment. The cash balance is likely to increase post IPO.

The Income Statement

Medline’s income statement is distinct from pure-play distributors because it captures both manufacturing and distribution margins.

Revenue (The Growth Engine):

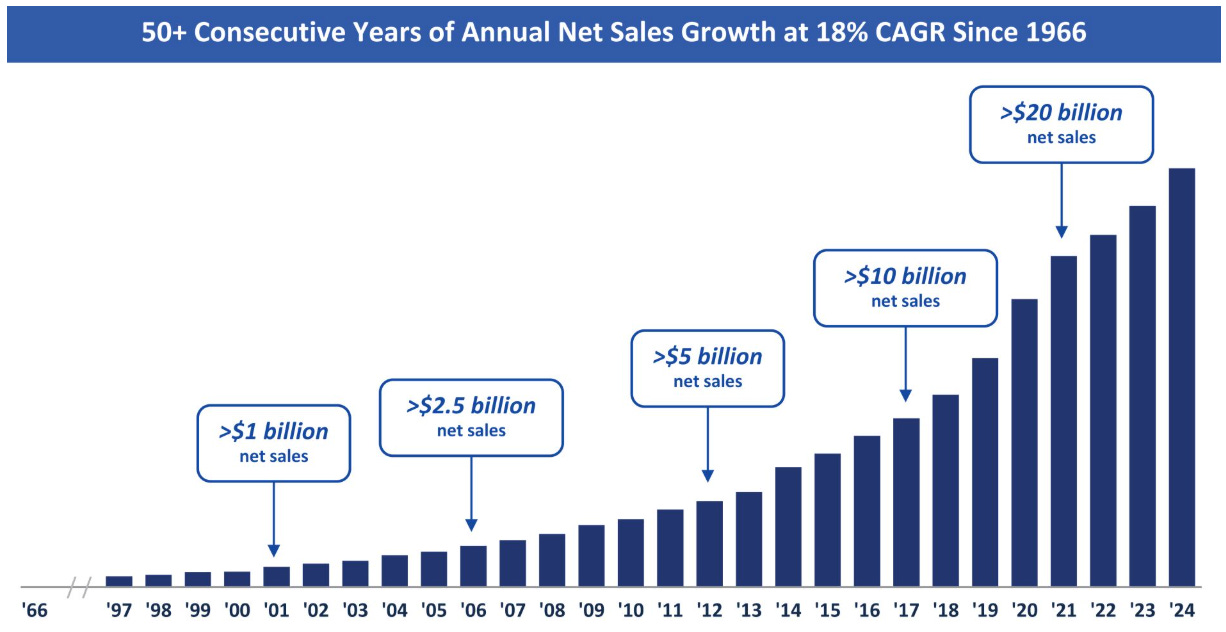

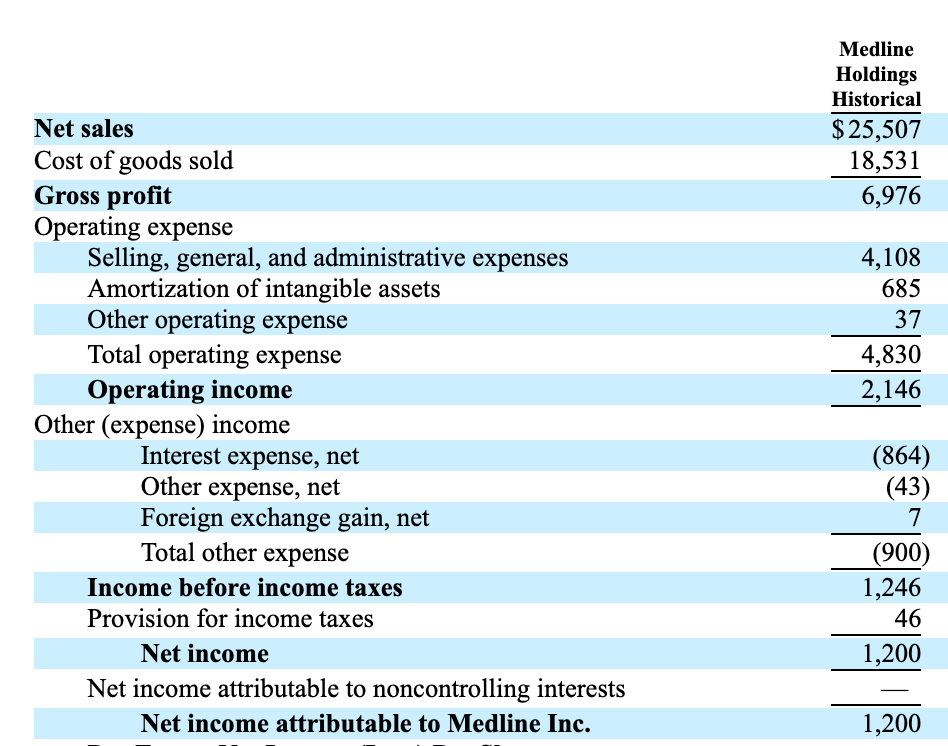

Medline generated $25.5 billion in net sales for the fiscal year 2024 and is on track for approximately $27.5 billion for fiscal 2025, representing high-single-digit-growth. Relative to historical growth, their revenue growth rate appears to be slowing.

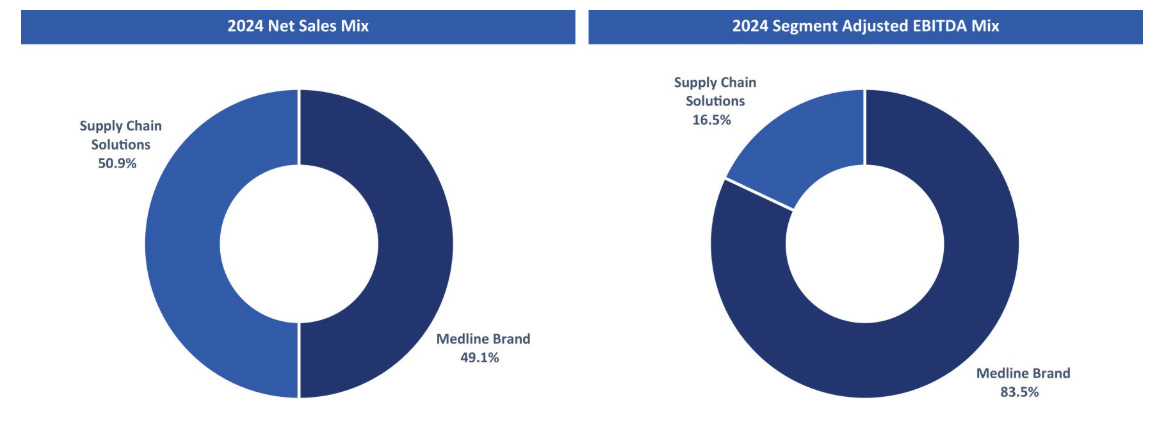

Revenue is split roughly 50/50 between “Medline Brand” products (proprietary manufacturing) and “Supply Chain Solutions” (distribution of third-party products).

About 93% of the revenue comes from the United States while the remaining 7% comes from International operations.

Profits:

Management is quick to tell investors that the “Medline Brand” segment generates over 80% of the company’s Adjusted EBITDA due to its superior margin profile, although they do not break this out on a GAAP basis.

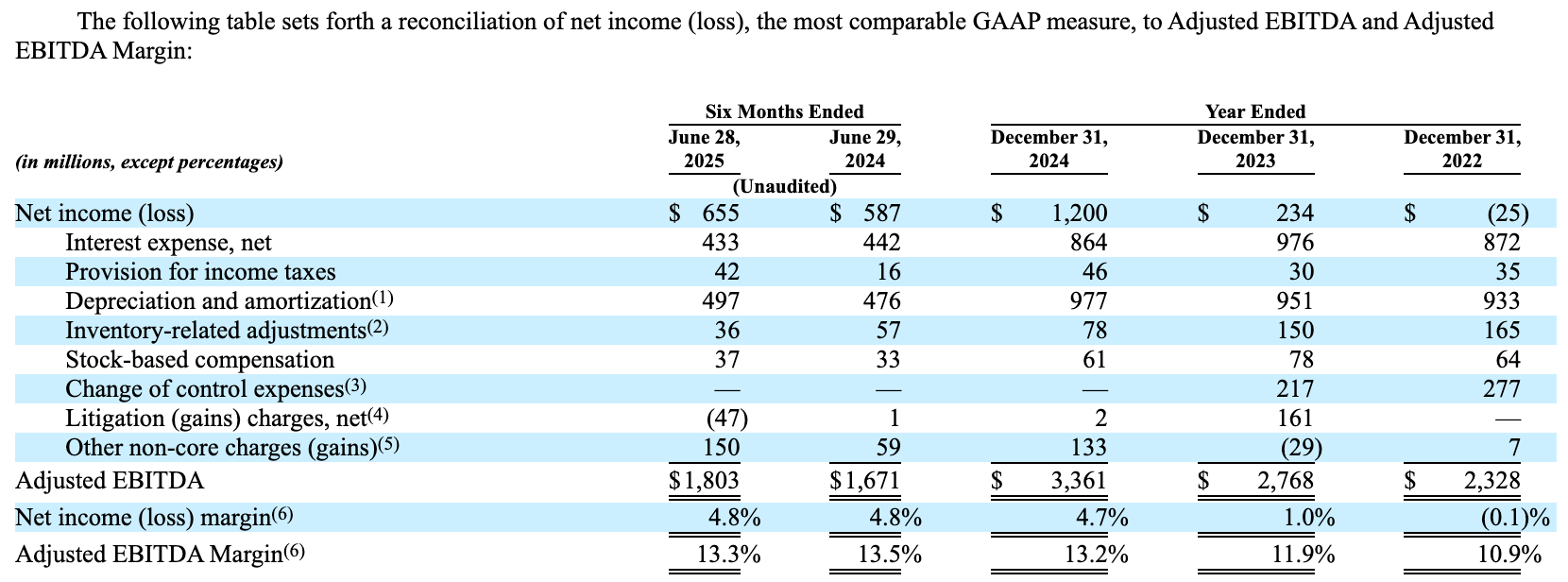

Their adjustments to EBITDA include:

Source: Medline S-1 - footnotes on page 115 and 116 of filing

While some adjustments may be considered reasonable (eg inventory adjustment for LIFO accounting), some (like stock-based comp, or litigation charges to protect valuable IP) are not. We will let the reader judge for themselves.

On a GAAP basis, operating margins come in at about 8%. This is substantially better than their pure play distributor competition, which has operating margins of 1-2%. Adjusted EBITDA margins are at about 13%.

For Fiscal 2024 management generated $1.2 billion of Net Income on $25.5 billion of revenue, for Net Income Margins of about 5%.

Moving forward, Management has guided for a $325 million to $375 million hit to 2025 pre-tax income driven by new trade tariffs. This is a material drag that will impact the P&L moving forward.

The Cash Flow Statement

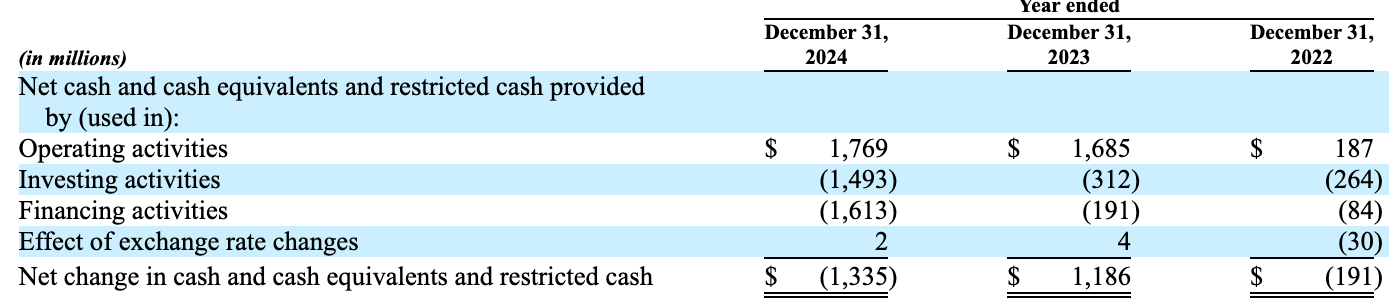

This is arguably the most attractive aspect of the financials. Once the debt service expense is reduced, Medline should become a prolific generator of cash.

Operating Cash Flow (OCF):

Medline generated $1.77 billion in cash from operations in 2024. This was a massive improvement from $187 million in 2022, largely due to stabilizing working capital after the pandemic supply chain disruptions.

Financing activities are a substantial drag and we can see that it eats up 91% of operating cash flow. Only $63 million of this is the repayment of debt, while $1.2 billion is due to “payment of additional tax distributions to certain partners to catch up on a pro-rata basis tax distribution previously paid to other partners”, as per their S-1.

It’s worth noting that in a partnership (LLC/LP), the company doesn't pay income tax; the owners do. These "distributions" were essentially the company paying the owners' tax bills for them. Post-IPO, Medline Inc. will pay taxes directly. It’s not necessarily “milking” in the predatory sense, but rather a structural requirement of pass-through entities.

CapEx is relatively “asset-light” for a manufacturer, running at $364 million in 2024. Because Medline has already built its massive logistics network (29 million sq. ft. of warehouse space), it does not need to spend aggressively on new infrastructure to grow. This leads to high free cash flow conversion.

Free Cash Flow (FCF)

Operating Cash Flow ($1.77B) minus CapEx ($364M) equals Levered Free Cash Flow of roughly $1.4 billion for 2024. On $25.5 billion of revenue this is a FCF Margin of 5.5%.

The ~$300 million in interest savings post-IPO will flow to Free Cash Flow in 2026. As debt is paid off, Free Cash Flow will continue to grow. This gives the company significant “dry powder” to resume acquiring smaller medical product manufacturers (M&A), or to return capital to investors.

The IPO: The Mechanics of the “Up-C” Structure

The S-1 details a series of transactions referred to collectively as the "Corporate Reorganization" and "Offering Transactions”. The IPO is not a simple conversion of LLC units into C-Corp shares. It is the implementation of an "Up-C" (Umbrella Partnership C-Corporation) structure, a sophisticated framework designed to bridge the gap between the tax efficiency desired by legacy owners and the corporate governance required by public markets.

In a standard IPO, the operating company converts into a C-Corporation and sells shares. In an Up-C, the operating company remains a flow-through partnership.

Medline Inc is the public company. This is a newly formed Delaware corporation that acts as the registrant. It has no operations of its own. Its primary asset is a controlling equity interest in Medline Holdings, LP. It issues Class A Common Stock to public investors - this is what trades under the ticker MDLN.

Meanwhile, Medline Holdings, LP is the OpCo. This entity holds all the assets, liabilities, and operations. It is the flow through partnership in the Up-C transaction. It continues to be treated as a partnership for tax purposes (meaning, it itself doesn’t pay any taxes but instead flows through profits and losses to holders, who then have to pay taxes).

Common Units are the privately held shares of Medline Holdings LP. The Offering Transaction involves the mathematical translation of the legacy “Partners’ Capital” classes (A, B, CUPI) into the new “Common Units” of the Up-C structure. If we look at the fully diluted share count of Medline Inc, we see there are just shy of 800 million fully diluted shares outstanding. As their IPO was for about 248 million shares, this means that 69% of the company (~ 550 million shares) is held as Common Units.

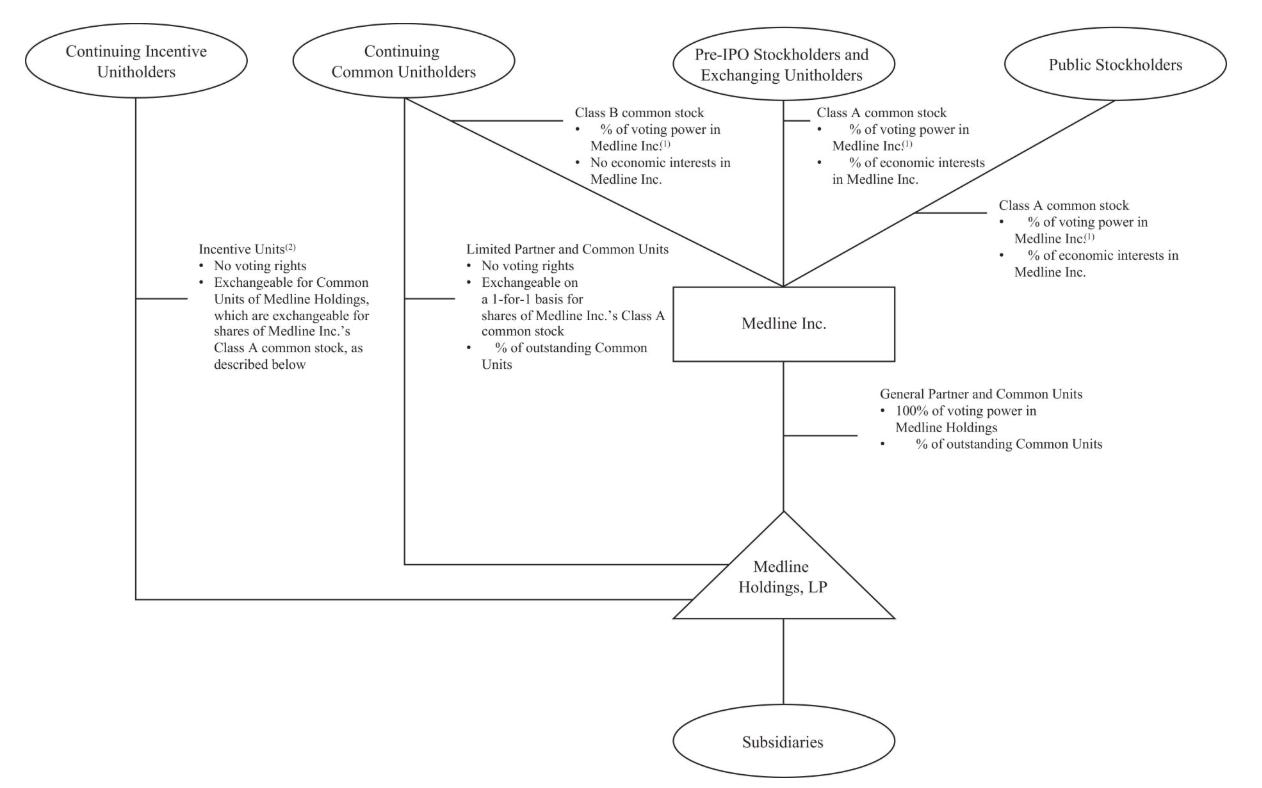

The S-1 outlines this “simplified” diagram to explain the post IPO structure:

The Continuing Incentive Units management incentives - stock based compensation - from when Medline was a fully private company. They can be converted into Common Units.

The Continuing Common Unitholders are the pre-IPO owners (Class A, Class B, Class B CUPI shareholders). Instead of exchanging their partnership units for PubCo stock (which would be a taxable event), they retain Common Units directly in Medline Holdings, LP. However, they are not trapped in the Common Units.

The Exchange Agreement

To provide future liquidity for the Continuing Common Unitholders, the structure includes an Exchange Agreement. Continuing Unitholders have the right to exchange their Common Units for shares of Class A Common Stock on a one-for-one basis.

This exchange can usually be triggered at the discretion of the unitholder (subject to certain blackout periods). When an exchange occurs, the partnership unit is cancelled, and Medline Inc. issues a new public share. This mechanism ensures that the legacy owners that have a permanent bridge to the public markets, allowing them to monetize their stake over time without forcing the entire company to sell.

What happens if the Continuing Common Unitholders (the Mills family and Private Equity firms) - who hold roughly 69% of the total company - decide they want a liquidity event and decide to swap to Class A shares all at once?

Supply - not Economic - Dilution

In a traditional sense, dilution happens when a company issues new shares to raise money, slicing the pie into smaller pieces. In the post IPO structure, the “pie” is already divided into ~799 million slices. The public owns ~248 million slices, and the legacy Private owners own ~551 million slices.

When a PE firm exercises its right under the Exchange Agreement, it hands over a private unit and gets a public share. The total number of slices (~799 million) remains exactly the same, and the MDLN holding public investor does not see their total ownership of the company shrink.

However, while number of shares remains the same, the supply of tradable shares increases with every conversion.

The current float consists of only 248 million shares. Over the next 12–24 months, as the private equity firms (Blackstone, Carlyle, H&F) exit, they will convert some, or all, of their 551 million units into Class A stock and sell them.

This effectively triples the supply of stock available in the market. If buyer demand doesn’t triple to match it, this wall of selling can put downward pressure on the share prices. This is often referred to as a “PE Exit Overhang.”

Tax Receivable Agreement (TRA) Friction

Medline Inc. has entered into a Tax Receivable Agreement with pre-IPO owners to pay them 85-90% of the tax benefits realized from the step-up in basis of assets.

Step-up in basis of assets is a U.S. tax rule where the cost basis of an inherited asset is adjusted to its fair market value. In the context of the Medline IPO, "step-up in basis" indicates an increase in the tax value of the company's assets, including goodwill and intangibles, stemming from a reorganization linked to the IPO.

By increasing the fair market value of the assets, Medline can then claim higher D+A on their income statement. These increased non-cash expenses then create a substantial future tax shield for the company. As they are non cash expenses, they would then flow through to the cash flow statement.

However, due to the TRA, that cash is then paid out to the pre-IPO owners, funneling cash back to the PE sponsors and founding family.

Now that we’ve gone through the business and their financial statements, let’s take a deeper look at Medline through our Four Pillars of Quality. After that, we’ll discuss risks, valuation, and provide a final verdict.