The Four Pillars of Quality

On Management, ROIC, Moats, Optionality and Reinvestment, and why Hermès is the prototypical example

Introducing the Quality Framework

Welcome to the inaugural post of The Pursuit of Compounding 📈

For too long, investing has been overcomplicated. It doesn’t have to be. Here at the Pursuit of Compounding We are focusing on one simple, powerful concept: Quality.

We believe Quality is the North Star for compounding. Simply put, quality inputs, plus time, compound into quality outputs. This is true in health (kale vs. soda; exercise vs Netflix), relationships (care and attention vs. neglect) business (win/win vs. win/lose), and finance.

We define a “Quality Company” as one that is run by ethical, long-term focused owners who can consistently generates high returns on invested capital, is protected by a wide, deep moat, and who have great opportunities to reinvest their profits.

Today, we’ll expand further on this four-point framework that we’ll consistency use for all our analysis, and then we’ll launch into a case study of one of our favourite portfolio holdings: the prototypical Quality Company and the French luxury house, Hermès International (RMS.PA).

The Four-Pillar Quality Framework

Created by author

We use Quality as a proper noun (hence capitalization) Why? Because Quality in this context is a distinguished trait that not all things possess. For example, the Mona Lisa would possess this trait. You know it when you see (or feel) it.

Before we dive into Hermès, let’s establish the Quality blueprint. We are looking for companies that score highly on all four of these essential pillars.

Pillar 1: Exceptional Management & Culture

Management is the most important, and most under-rated factor. Finance generally has a bias to the quantitive aspects of business - What is the revenue? What are the earnings? What are the cash flows? However, these quantitive factors are the outputs of qualitative factors of the business. Humans ultimately make the decisions that lead to the numbers. Said another way, financial statements tell you what happened; management and culture tell you why it happened and what will happen next.

Thus, we start by looking for a long-term, owner-operator mentality, deep domain expertise, and a culture that prioritizes the product, the customer, and the craft. These are factors are more valuable than the underlying numbers of the company, as these are the factors that drive long term compounding.

Arguably, we believe this is the single hardest part of investing, as this is a relatively ineffable factor that sustains long term compounding, and produces the outputs we all love (high returns on capital and growth). Although, if absent, the high returns and growth tend to be fleeting, rather than sustained.

As Robert Pirsig explains the Metaphysics of Quality:

“Quality is not a thing or a quality that is applied to things, but rather the fundamental source from which both mind and matter emerge.”

In the finance context, mind and matter would be replaced with underlying fundamentals and long term growth.

Again, we have to state that this is the most important - and often most overlooked - aspect of investing. Poor management and poor culture will destroy any business in the long term.

Pillar 2: High Returns on Invested Capital (ROIC)

ROIC measures how effectively a company uses the capital (debt and equity) entrusted to it to generate profits. For example, if a company invests $100 in a business line and this business then goes on to generate profits of $20 the ROIC is 20%. Consistently high ROIC a gold standard that we look for - it proves the business is not a commodity and has real, measurable economic power.

We love high ROIC for three main reasons - it’s a sign of disciplined capital allocation, it enhances long term growth, and it provides optionality.

Disciplined Capital Allocation:

We talked about the importance of management, as the long term economic success (or failure) depends on human decisions. Quality decisions lead to high ROIC, while the opposite is also true. Sustained high ROIC is one sign that management has a track record of capable and competent business decisions, and that we can trust them with our capital.

Long Term Growth:

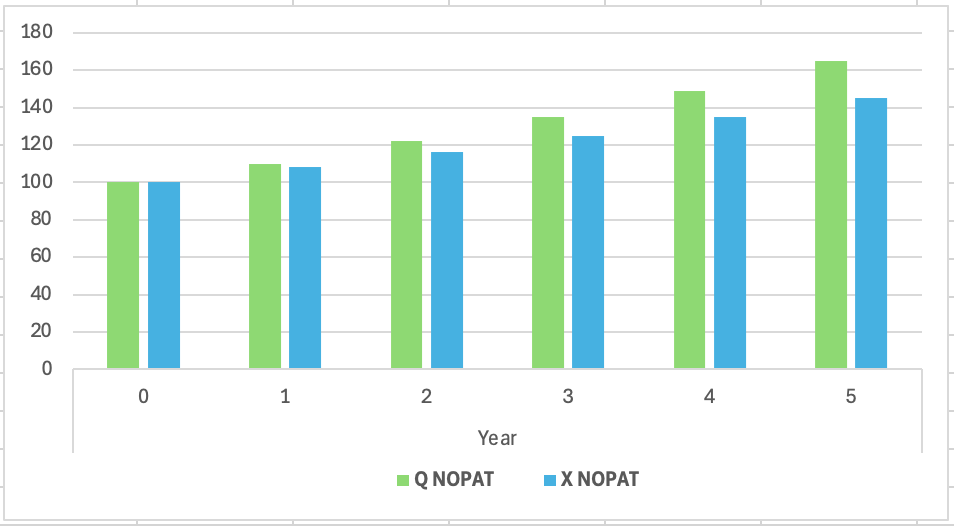

As an example, Company Q and company X both operate in the same industry. Company Q has a historical ROIC of 20%, while Company X has a historical ROIC of 15%. At the outset, both reinvest 50% of their revenue into further growth initiatives.

Both have a starting Net Operating Profit After Tax (NOPAT) of $100.

Table 1: NOPAT of Q and X over 5 years (compounded at ROIC x reinvestment rate)

Figure 1: NOPAT of Q and X over 5 years (compounded at ROIC x reinvestment rate)

Even though both companies started at the same point, and despite an only 5% delta in ROIC, after 5 years Q has a NOPAT that is already 13% higher than X.

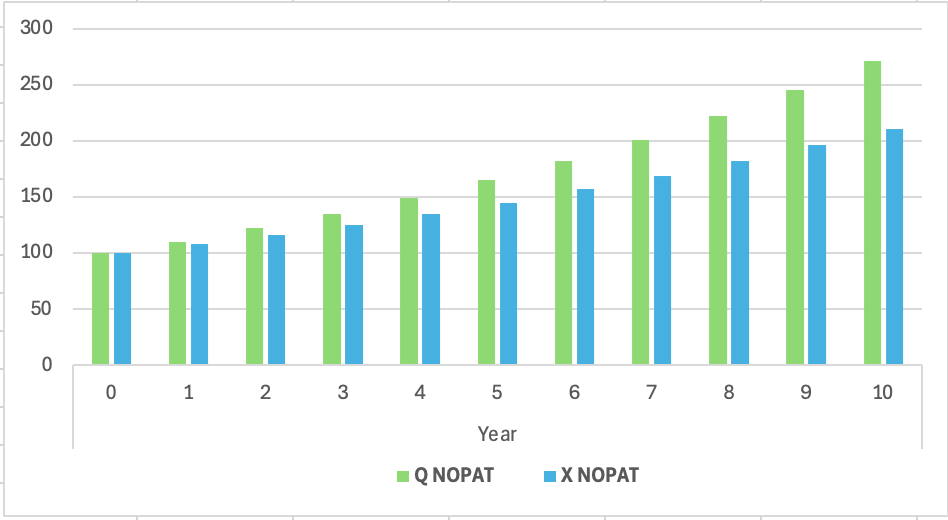

The longer Company Q outcompetes X, the wider the delta becomes. For example, after 10 years compounding at the example above, the delta between NOPAT for Q and X would have increased to 28%, despite the ROIC difference between Q and X being fixed at 5%.

Table 2: NOPAT of Q and X over 10 years (compounded at ROIC x reinvestment rate)

Figure 2: NOPAT of Q and X over 5 years (compounded at ROIC x reinvestment rate)

We have to recall that outputs - like ROIC and NOPAT - are a result of inputs. Thus, if Q can sustain higher ROIC than X, it’s business is better, which likely means it’s gaining market share or unlocking opportunities faster than X cannot. This is what long term sustainable growth is all about.

A high ROIC isn’t enough by itself though, as data does show that most companies with ROIC eventually revert to the mean. This makes sense, as high returns on capital subsequently attracts capital, and this increases competition. Increased competition has the potential to then lower returns on capital.

Pillar 3: Defensible Business Model (The Moat)

A Quality business is a protected one. To sustain compounding in the long term, its advantage must be structural, not fleeting. The business model must be defensible. Common examples include Regulatory, Barriers to Entry, Intangible Assets (Brand), Switching Costs, Network Effects, or a Scale Economy / Cost Advantage. The ultimate goal is a business model that is structurally insulated from competition.

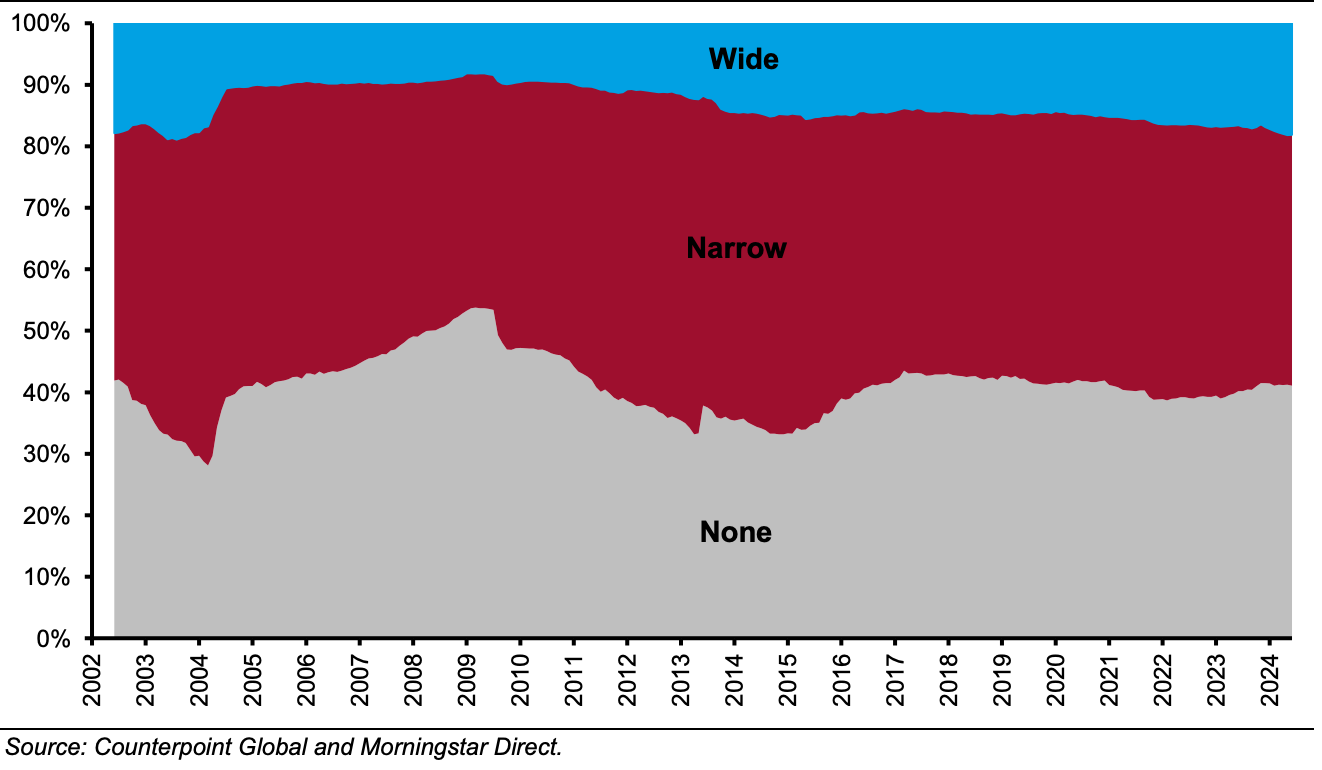

However, not all moats are created equally, many businesses have no moat at all.

Figure 4: Distribution of Morningstar’s Economic Moats Rating - 2002 - 2024

A Quality company, by definition, has a wide moat. We must be mindful though that the moat does not create the Quality company; the Quality company and the factors that make it a Quality company create the wide moat.

Just like ROIC, a moat is an output that is generally created by the actions of the people running the company. Even if the moat is regulatory, corporate actions are still responsible for maintaining the moat by continually complying with regulation.

And, management actions also dictate where excess cash flows are re-invested.

Pillar 4: Opportunity to Reinvest Cash Flows

A Quality businesses’ super power - and what creates the long term value creation we at TPQ desire - is it’s ability to reinvest it’s cash flows at high rates of return. A high-ROIC business will not compound if it has no opportunity to re-invest for future growth. For example, in the example above, Company Q instead paid out 100% of it’s NOPAT to it’s business owners, then it’s NOPAT would not grow with time, and subsequently the intrinsic value of the Q would not increase.

Quality companies are compounding machines— they take their copious free cash flow, reinvest it back into the business at high ROIC, and drive exponential profit growth for decades.

Even if the reinvestment opportunity is not immediately apparent, Quality companies often have high optionality and can create new investment opportunities to continually reinvest. This is a wonderful byproduct of partnering with exceptional managers and again highlights the importance of partnering with the right people for the long term.

Optionality

Recall the 10 year example above, with Company Q and X. Company X is inferior to Q, which manifests with a lower ROIC. Thus, to keep pace with Q, X has to reinvest a higher portion of its NOPAT (eg reinvestment rate has to increase) to maintain parity. This provides less financial resources to pursue other initiatives.

On the other hand, as Q is superior to X, it has to reinvest a lower portion of its NOPAT to keep pace with X, thus allowing it to focus on other areas (R&D, acquisitions, etc).

As we already know that Q is run by disciplined capital allocators, any subsequent areas of reinvestment at a superior ROIC will continue to build the compounding flywheel.

An example is the current TPQ holding - Amazon (AMZN). Amazon exercised it’s optionality. It began investing into Amazon Web Services (AWS) in 2005 / 2006 and helped kicked off the cloud revolution. At the time, the future value of AWS would not have been apparent to Amazon shareholders. However, because they partnered with a Quality company, optionality plus reinvestment led to immense value creation.

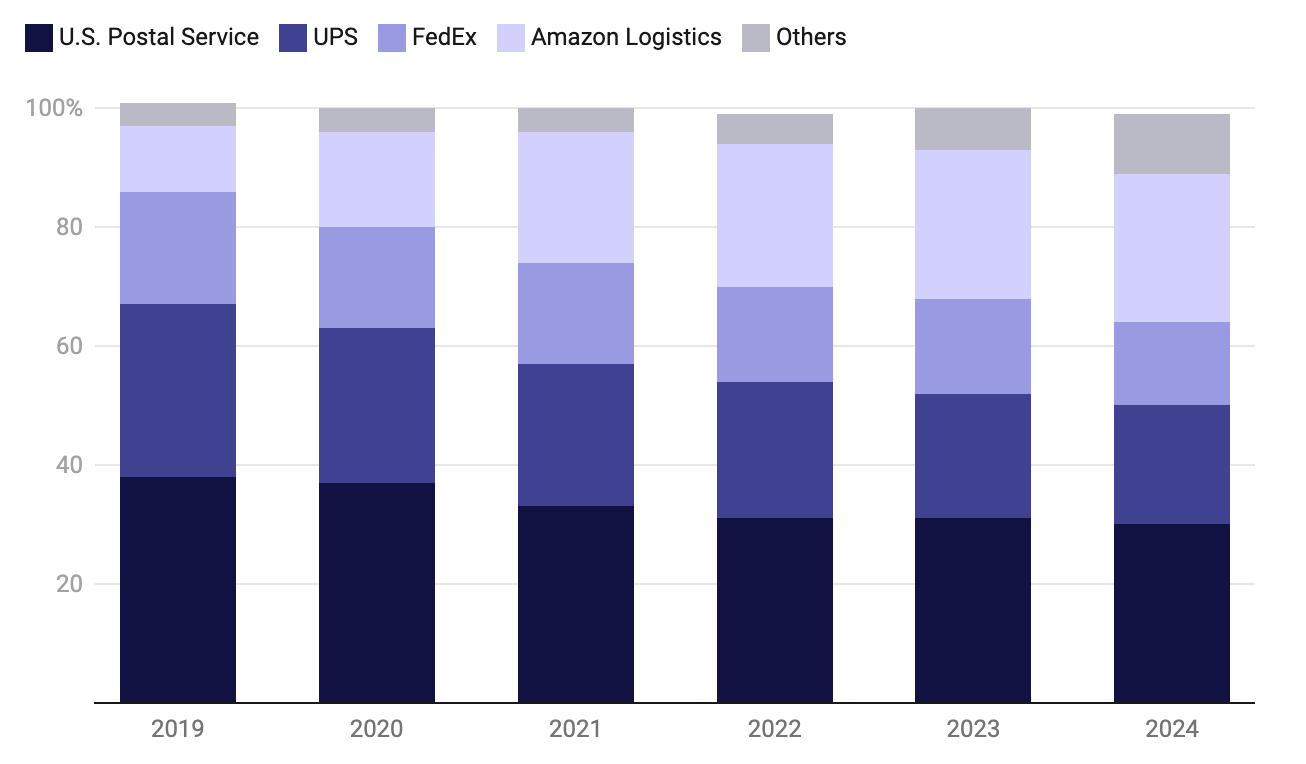

More recently, AMZN started to invest heavily in it’s logistics network in 2015, and since then has now become the second largest by market share in the US, supplanting both FDX and UPS. As of 2024, AMZN has 25% of the delivery volume share, second only to USPS (30%) while UPS is third (20%) and FDX is fourth (15%).

Figure 3: US parcel market data 2019 - 2024 - source SupplyChainDrive.com

A Quick Note on Valuation

We’ve intentionally put valuation at the end of the article, rather than the start, as for a long term investor - what investing isn’t long term? - valuation is the least important. Yes, you read that correctly - when buying and holding a Quality company, valuation is the least important.

”Time is the friend of the wonderful company, the enemy of the mediocre.”

Warren Buffett

All too often investors start with the valuation, rather then finish with it. Starting with the valuation implies that all companies are equal, and thus it’s a game of relative value selection. For example, Company X is “cheaper” than Company Q, therefore Company X is the better investment. We’d take the opposite side - Company X is an inferior company to Company Q, and thus it commands a lower intrinsic value. Often in markets, and in life, you get what you pay for.

To be a Quality investors we often have to pay up for Quality businesses - businesses that sometimes look insanely expensive optically on P/E or EV/EBITDA ratios. However what is lost is the nuance on the Management and Culture, the ROIC, the Optionality, and the Opportunities for reinvestment. Here, work has to be done to parse out the signal from the noise - is it “expensive” because it’s a Quality company? Or, because it’s the new hot thing that everyone wants to own?

We prefer to do discounted cash flow (DCF) analysis when doing a valuation for a quality company, as the terminal value is heavily influenced by the factors above. Said another way, the longer the runway, the more you can pay today for a Quality company and still get a satisfactory return.

Reverse DCFs are often helpful as well, as we can then get an idea as to the growth that is priced in today, and then judge if those market expectations are reasonable vs unreasonable.

This brings us to the final section - a quick case study to put the principles into action. We’ll look at a company founded in 1837 that’s still growing today: Hermés.

Simple Case Study: Hermès

Hermès is the ultimate example of a Quality business. It is a company built on scarcity, craftsmanship, and a complete refusal to compromise its values for the sake of volume. Let’s run it through our four-pillar framework.

")

1. Exceptional Management & Culture

Hermès has been family-controlled since its founding in 1837. The current CEO, Axel Dumas, is a sixth-generation descendant.

The Long View: All decisions are geared toward preserving brand quality and mystique, not maximizing the next quarter’s sales. They refuse to automate and strictly limit production.

The Artisan Focus: Hermès sees itself as a house of artisans. It employs thousands of craftspeople and has its own École Hermès des Savoir-Faire (School of Know-How) to ensure the next generation of French leather workers is ready. This is a commitment to a craft that money can’t buy.

2. High Returns on Invested Capital (ROIC)

The financial results are staggering, a direct outcome of their focused culture.

Profitability: In fiscal year 2024, Hermès reported an operating margin of 40.5% on €15.2 billion in revenue. This is a level of profitability few companies in the world can touch, even in luxury.

Economic Proof: A recurring operating margin over 40% combined with a net margin around 30% points to an extremely high, consistent ROIC, likely well north of 25-30% year after year. Their capital is exceptionally productive.

3. Defensible Business Model (The Moat)

Hermès’s moat is arguably the widest and deepest in the luxury world, built on a paradoxical strategy of deliberate constraint.

The Ultimate Intangible Asset (Brand): The Hermès name, and especially the Birkin/Kelly bags, has moved beyond a simple brand into a genuine store of value. These bags appreciate on the secondary market for 2x to 4x their retail price. This scarcity attracts the most resilient customer base: the ultra-high-net-worth individual.

Vertical Integration & Know-How: The company owns its production process. The fact that a single artisan makes a single Birkin bag over 20+ hours is a quality control moat. When competitors try to replicate the process, they discover that Hermès essentially employs the world’s supply of craftspeople capable of this level of work.

4. Opportunity to Reinvest Cash Flows

A fantastic company is only a fantastic investment if it can continue to grow. Hermès has two primary, high-ROIC avenues for reinvestment:

Expand Production Capacity: The main limit to growth is production capacity. Their constant investment is in new, hyper-local leather goods workshops across France. This capital is deployed to train more artisans and build the infrastructure to meet some of the unquenchable demand—all at a very high return.

Expand the Exclusive Distribution Network: Hermès strategically opens and renovates new, directly operated stores in key global markets. These stores serve as the exclusive showcase for their products and, importantly, are a compounding hub where customers waiting years for a bag buy their highly profitable ancillary products (scarves, perfumes, ready-to-wear).

The Verdict

Hermès is a textbook example of a Quality company. It has exceptional leadership and culture that drives its strategy, which in turn creates its moat, and that moat generates exceptional profitability that can be strategically reinvested back into the business.

We own a position in Hermés, and this is the kind of compounding machine we want to continue to own forever.

Join us next time, as we continue our pursuit of compounding.

Happy Compounding,

The Pursuit of Compounding 📈

PS: Like what you read? Buy us a coffee!

Disclaimer: We are private investors and not financial advisors. This post is for educational purposes only and does not constitute financial advice. Amazon (AMZN) and Hermès (RMS.PA) are stocks we currently hold. Always conduct your own due diligence before making any investment decisions.

"Enzo Ferrari loved cars." Yes. But he did NOT love electric cars. No true car enthusiast does.